Publication

Motor Finance Redress: The Way Ahead

On August 1, 2025, the UK Supreme Court delivered its long-awaited judgment in Hopcraft v Close Brothers Limited and on 3 August the FCA announced it would consult on a redress scheme.

Global | Publication | June 2020

New research conducted by Norton Rose Fulbright shows that force majeure clauses are already being invoked in certain industries and regions but that this is not yet leading to a domino effect to drag in other industries and regions. Our statistical analysis reveals some intriguing trends on the use of and reaction to the use of force majeure clauses.

‘Force majeure’ refers to unexpected circumstances outside a party’s reasonable control that prevent it from performing its contractual obligations. Some legal systems excuse performance in these circumstances (e.g. France). Although force majeure is not a standalone concept in English law, many English law contracts include force majeure clauses that are intended to achieve a similar result. There is widespread speculation that COVID-19 will lead to parties to contracts invoking force majeure. Companies may be studying their local markets, waiting to see if one counterparty relies on force majeure and if this leads to its use generally. Accordingly, information about how contractual counterparties are acting in the market and what is influencing them is vital.

Norton Rose Fulbright conducted a groundbreaking survey and analysis of the global spread of force majeure in April 2020, showing that force majeure clauses were being invoked in some industries and regions, but that this was not yet leading to a domino effect dragging in other industries and regions. A new update to the survey shows that this remains true, and provides further independent confirmation of the trends we originally identified.

The original survey consisted of 248 individual survey responses from corporates and financial institutions on April 2, 2020. Norton Rose Fulbright conducted a follow-up survey on 27 May, 2020, obtaining a new set of 168 responses. The results of the original analysis were verified for this new set of data. In particular, the main conclusion from the original analysis, that whether a party was considering force majeure depended on whether it had used it before and not on whether its counterparties had used it, was still valid. This is strong additional evidence for the original conclusion and also suggests that this behaviour has not yet changed. Corporates and financial institutions should take account of this market intelligence when managing their own contracts and dealing with their counterparties.

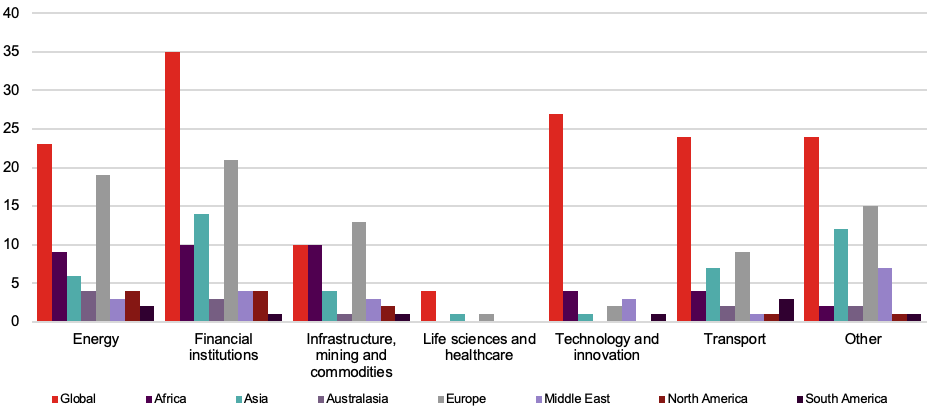

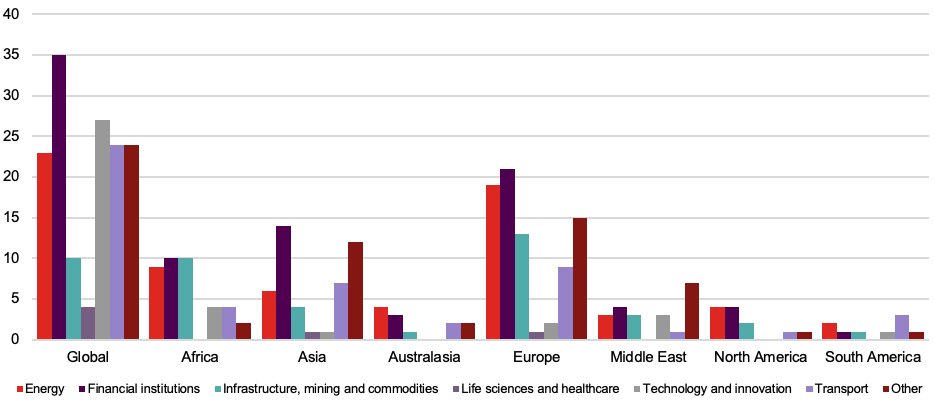

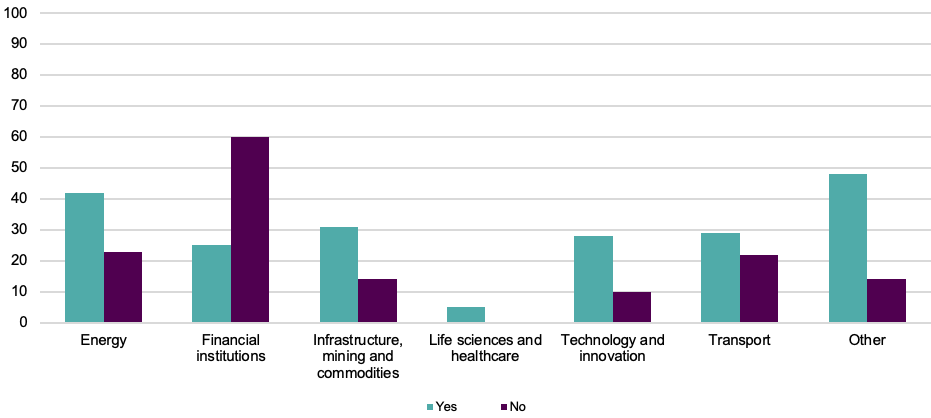

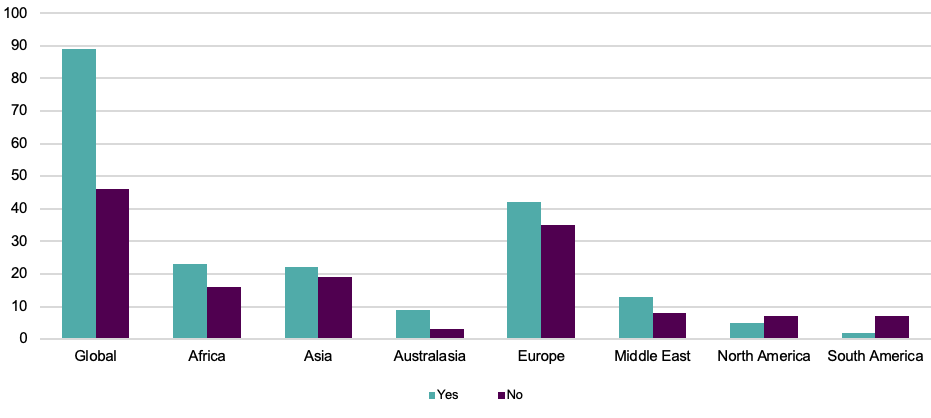

Norton Rose Fulbright obtained 248 individual survey responses from corporates and financial institutions on April 2, 2020. Polling was undertaken with named individuals in senior positions at those institutions, which were spread across different industry sectors and all geographical regions. The industries most represented were finance (24 percent) and energy (18 percent) and the industry least represented was life sciences (2 percent). Respondents operating globally accounted for 42 percent of the total; regions were represented from Europe (25 percent), the highest, through to the Americas (5 percent) and Australasia (4 percent), the lowest. For a breakdown of respondents by location and industry in more detail, see Figure 1.

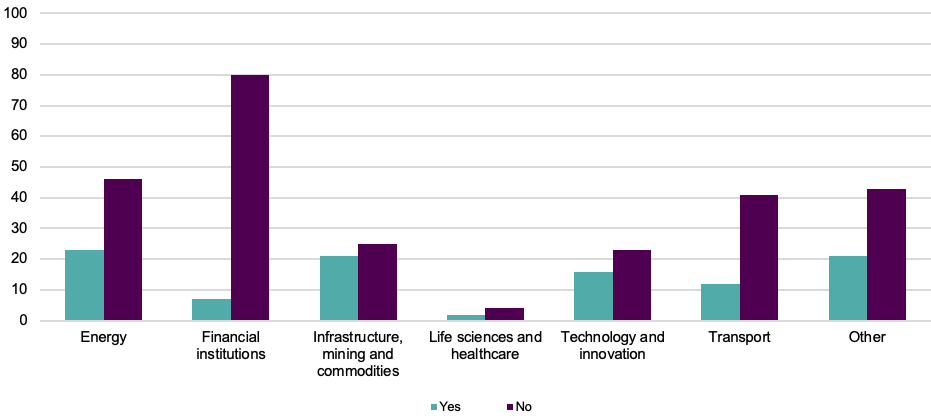

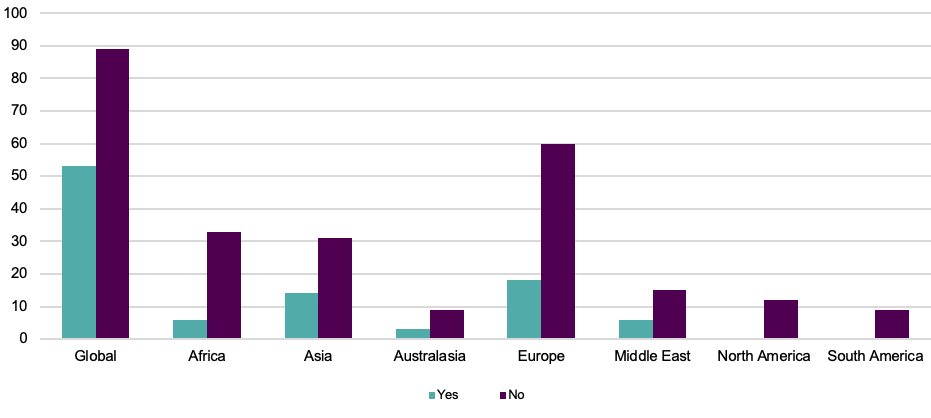

Nearly a third of all respondents had relied on force majeure themselves in 2020 (31 percent). However, just over half had experienced a counterparty relying on force majeure (56 percent) and nearly two-thirds were considering using it in the future (62 percent). For a breakdown of reliance on force majeure and consideration of force majeure usage by both industry and location, see Figures 2 – 5.

The main results of the analysis are as follows (for details of methodology, see the Appendix):

Overall, the survey shows a pattern of geographical and sector-specific invocation of force majeure. But use of force majeure does not appear to be spreading merely by contact: what determines whether a company is considering invoking force majeure is not whether one of its counterparties has invoked it, but whether it has relied on force majeure previously itself. So, for now, force majeure remains concentrated within certain markets.

Companies will need constantly to evaluate the legal and commercial risks of force majeure being invoked by them or against them. Legal risks include being found in repudiatory breach of contract for wrongly invoking force majeure; commercial risks include the effect of force majeure on interdependent supply chains. Conformance to market norms is a key overall part of that risk evaluation. Norton Rose Fulbright aims to provide continuing market intelligence, such as by the current survey, to help advise on that risk evaluation and its consequences.

Data was analyzed using a multivariate logistic regression supplemented by a random effects model to account for clustering by individual respondent and corporate entity. Calculations were performed in R and the glmmML library was used. There was no imputation of missing values.

Univariate logistic regression was used for initial investigation. Then stepwise selection within a multivariate regression was used to obtain the final model. Robust p-values were obtained by a bootstrapping analysis using the original data. Positive results were reported at a p-value threshold of 0.05, although in practice the largest p-value of all results referred to in the main text was 0.03.

Publication

On August 1, 2025, the UK Supreme Court delivered its long-awaited judgment in Hopcraft v Close Brothers Limited and on 3 August the FCA announced it would consult on a redress scheme.

Publication

The Regional Court of Munich (LG München I) has issued a landmark judgment in GEMA v OpenAI (Case No. 42 O 14139/24), holding that the use of copyrighted song lyrics for training generative AI models without a licence violates German copyright law.

Publication

Songa Product and Chemical Tankers III AS v Kairos Shipping II LLC [2025] EWCA Civ 1227 (07 October 2025) has clarified the extent of the obligation on the Charterer to redeliver a vessel following the termination of a Barecon 2001 charter and of the Owner’s right to require it to be redelivered to a port “convenient to them”.

Subscribe and stay up to date with the latest legal news, information and events . . .

© Norton Rose Fulbright LLP 2025