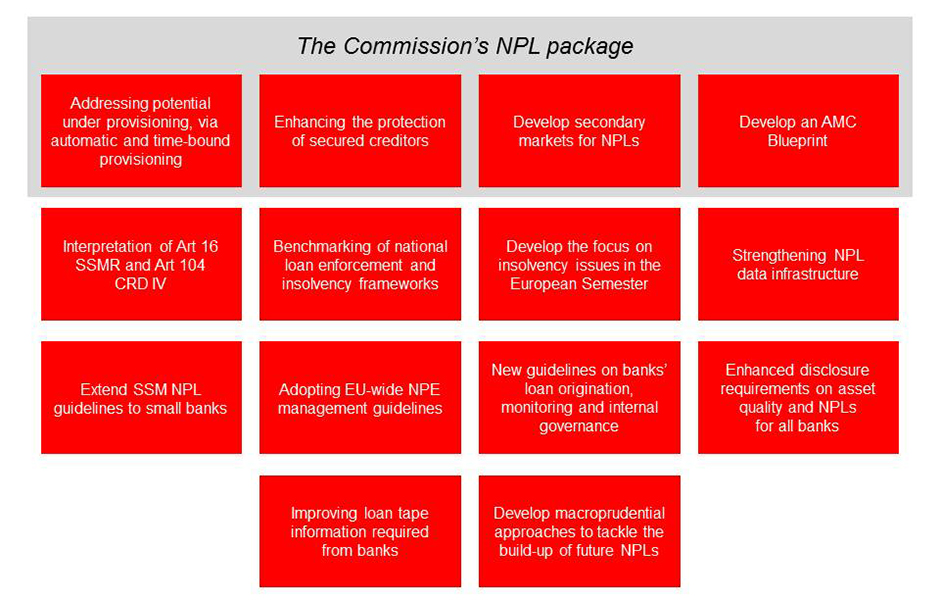

Essentially the draft Directive is intended to prevent excessive future build-up of NPLs on banks’ balance sheets. It does this in two ways. First, it encourages the development of an EU-wide secondary market for NPLs, by setting common standards for the “proper conduct and supervision” of credit servicing companies, specialist firms with the “necessary risk appetite and expertise” employed by banks to seek repayment of non-performing consumer and commercial loans. Second, by requiring each EU Member State to establish an AECE which is intended to be a faster way for banks to salvage bad business loans by recovering the collateral against which they are secured rather than through existing insolvency and debt recovery legislation.

In relation to the development of the secondary market for NPLs, the draft Directive creates a common set of rules that third party credit servicers need to abide by in order to operate. Such rules include

- The need to obtain authorisation from the home Member State regulator before carrying out credit servicing activities. Such authorisation would be dependent on the credit servicing company meeting conduct and organisational requirements.

- Authorised credit servicing companies will need an “appropriate policy” to ensure the “fair and diligent treatment” of borrowers whose loan agreements it services, including referring them to “debt advice or social services” where necessary.

Importantly, an authorised credit servicing company would be able to passport its services in any EU Member State. Supervision of the authorised credit servicing company would be the responsibility of the home Member State authority although authorities in host Member States could conduct checks, inspections and investigations in respect of credit servicing activities in their territory. The draft Directive does not provide for an equivalence regime for non-EU credit servicing companies.

Credit purchasing is another important component of the draft Directive setting out minimum disclosure requirements by the bank towards the prospective buyer of a loan agreement, as well as requiring the sale to be notified to the regulatory authority. Non-EU credit purchasers will need to appoint a designated representative in the EU before they can purchase a credit agreement involving an EU-based borrower.

In terms of accelerated collateral recovery, the draft Directive requires Member States to establish, in law, a “more efficient” method for banks and credit purchasers to recover money from secured loans to business borrowers without recourse to legal action in court. Recovery of collateral under the AECE will take the form of a public auction, private sale or outright appropriation of the asset by the creditor. The AECE will only be available when agreed on in advance by means of a loan agreement between the lender and the borrower, and could not be used in relation to secured consumer credit agreements, such as residential mortgages.

To ensure fair treatment, the draft Directive requires the creditor to have the assets independently valuated to determine the appropriate reserve price for auction or private sale (or its value to the bank in case of appropriation). The valuer needs to be appointed by common consent of both the lender and the borrower, and the collateral could only exceptionally be sold for less than the reserve price (and never for less than 80 per cent of the estimated value). Any positive difference between the selling price and the outstanding debt would revert to the borrower.