Publication

Vietnam’s shift to capacity and energy pricing: What the two component tariff means

The two-component tariff has been mandated in Vietnam pursuant to Article 50 of the amended Electricity Law 2024 and Government Decree 146/2025/ NĐ-CP.

Global | Publication | December 2016

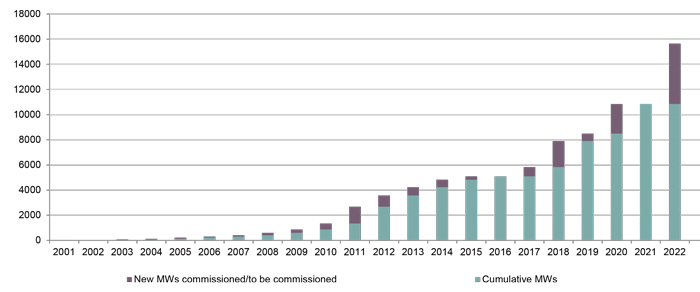

The UK is currently the world leader in offshore wind, with 5GW operational and targeting 10GW of installed capacity by 2020. The size of projects is increasing, enabling economies of scale to be captured. For example, in February 2016 DONG Energy announced its intention to proceed with construction of the 1.2GW Hornsea Project One offshore wind farm, which is set to become the world’s largest offshore wind farm (and is expected will use Siemens 7MW turbines).

The recent UK referendum vote to leave the European Union (EU) has sent ripples through both political and investment circles. In relation to offshore wind, the incumbent ministers were quick following the referendum to signal their intention to continue investment in clean energy, including offshore wind. For example, on June 29, 2016, Amber Rudd, the then Secretary of State for Energy and Climate Change, emphasised the continuing intention to bring forward more offshore wind, subject to cost reductions (as before). However, as new ministers take office, industry is pressing for a restatement of the previous Government’s policy by the newly constituted Department for Business, Energy and Industrial Strategy (BEIS). Despite the resulting political uncertainty, BEIS has confirmed that the next Contract for Difference (CfD) allocation round for less-established, ‘pot 2’ technologies, including offshore wind, will open on April 3, 2017 and it seems likely that offshore wind will be the primary beneficiary of that allocation round. For further information on the CfD 2017 allocation round, please see our briefing here.

Figure 1: MWs of offshore wind capacity commissioned or to be commissioned in Great Britain

Under many models for the withdrawal of the UK from the EU (other than using the European Economic Area (EEA) model), the UK would be released from its renewable energy targets under the EU Renewable Energy Directive. However, it is highly likely that renewable electricity will form part of the future energy mix. This is because the indications are that the UK still plans to comply with its national emission reduction targets under the Climate Change Act 2008 and its international climate change obligations (although these obligation will need to be disentangled from those of the EU). On July 20, 2016 (almost a month after the referendum result) the Carbon Budget Order 2016 came into force, enshrining the 5th Carbon Budget covering the period 2028-2032 at an equivalent 57 per cent emission reduction on 1990 levels into law. In addition to climate change considerations, there are other powerful drivers for renewable energy development such as security of supply and environmental benefits.

How much of this renewable energy development will be met by offshore wind will be (as before) determined by national renewable energy policy. Statements by the former Secretary of State for Energy and Climate Change, Amber Rudd, and the former Minister for Energy, Andrea Leadsom, confirmed the UK Government’s ambition to support up to 4GW of offshore wind and other technologies for deployment in the 2020s – providing the costs come down. Whilst Theresa May’s new cabinet have been slow to publish their views on the UK energy mix, a picture is beginning to emerge which promotes nuclear power, offshore wind and new gas-fired generation. The Secretary of State responsible for BEIS, Greg Clark, has made statements supporting offshore wind and recognising that it will have a ‘big role to play’1. Following announcements regarding the shape of the second CfD allocation round, which will open in April 2016, it appears that offshore wind will be the principal beneficiary of that funding round.

In the United Kingdom, we are currently in the process of moving from one support mechanism to another. The old mechanism (that will continue to apply to projects that have already accredited under it) is the RO (a ‘green certificate’ scheme). It is being replaced with CfDs, a revenue stabilisation mechanism which in broad terms fixes revenue at a contractual strike price and which are allocated competitively.

For Brexit to take effect, the European Communities Act 1972 (ECA), which provides for the supremacy of EU law, will need to be repealed. Repealing the ECA would bring an end to the constitutional relationship that exists between EU and UK law. Moreover, the vast amounts of secondary legislation that have been passed with the objective and justification of implementing EU law would have to be considered by Parliament. For further information see the UK and EU legal framework section of our Brexit client site.

The eventual repeal of the ECA will not affect the CfD legislation, which has the Energy Act 2013 as its enabling legislation. However, because aspects of the Renewables Obligation Order 2015 (ROO) which governs the RO rely on the ECA as the primary implementing legislation, the UK Government will need to take some positive action upon repeal of the ECA to preserve the legal basis for the ROO. Whilst we consider this to be a formality, it is nevertheless important that the UK Government manages the repeal of the ECA so as to preserve rights to support under the RO. The ROO is not the only secondary legislation affected in this way. Given the volume of legislation affected, the Government is considering a Great Repeal Bill to grandfather existing regulatory regimes, retaining EU legislation which could then be amended or repealed as appropriate at a later date. For further information on the Great Repeal Bill, please refer to our blog post ‘The Great Repeal Bill’ here.

In many Brexit scenarios (other than the EEA model), the UK will be released from State aid rules which have been influential in shaping the RO and CfD support regimes. Both regimes have already received State aid clearance, and therefore, Brexit is unlikely to have any immediate impact. However, if the UK were no longer bound by EU State aid rules, the Government may have more freedom in both the design and phasing out of renewable energy support regimes. The UK support regimes would however be open to bilateral responses from countries that might believe that any subsidies run counter to principles under the WTO regime, although WTO rules restrict the actions which WTO members can take to counter the effects of subsidies.

In the longer term, investors will also wish to consider how any changes in law introduced as a result of Brexit will affect the project’s power purchase agreement and/or CfD. However, this analysis will only be able to be carried out once any such changes are proposed. Under a typical power purchase agreement, change in law provisions broadly seek to preserve the balance of risk and reward between the contract counterparties following the change in law. The CfD also includes change in law provisions, recognising that for example, if a change in law results in an increase in project costs, generator profits may be eroded as, once the contractual strike price is reached, a generator will not benefit from the ability to recover these costs from consumers via higher electricity prices.

The UK offshore wind market has historically attracted a lot of interest from overseas investors. Merger control will be an important consideration for prospective investors in the UK offshore wind market. If the UK remains part of the EEA, rules equivalent to those under the EU Merger Regulation would continue to have potential application to mergers, acquisitions and joint ventures in the UK under the EEA Agreement. In any other scenario, EU-based investors in the UK market would need to consider the application of UK merger control rules. In some cases, both sets of rules might apply. For further information on the impact of Brexit on antitrust and competition, see our Brexit client site.

An offshore wind project with an existing funding commitment from both EIB and commercial lenders, is unlikely to be in breach of its credit agreement directly as a result of the referendum vote or indeed the eventual withdrawal of the UK from the EU. It is unlikely that a specific provision relating to the UK’s continued membership of the EU is included in the documentation. However, investors and funders should monitor indirect triggers which are often included in credit agreements and, depending on how withdrawal negotiations play out, may be triggered at a later date.

For example, many credit agreements contain material adverse change clauses; clauses which consist of representations or events of default relating to an event or circumstance (for example a change in law) which has (or is reasonably likely to have) a material adverse effect (MAE). The drafting of these varies widely and is often heavily negotiated, so whether a MAE is triggered by the eventual withdrawal of the UK from the EU will depend on the terms of that particular clause. This can often lead to problems in interpreting provisions of the finance documents themselves. Recent guidance2 on material adverse change clauses has distilled a number of principles including that (i) the ‘financial condition’ of a company alone does not encompass external economic or market conditions, but primarily its accounts and other financial information, (ii) whether a change is material depends primarily on whether it will affect the relevant party’s ability to meet its obligations under the agreement and (iii) an event which is known at the time that a contract is signed, such as Brexit, cannot of itself be a material adverse change.

At the time of writing, there has been no change to English law as a result of the Brexit vote. However, it is anticipated that regulatory change will follow in the medium to long term as the UK seeks to decouple itself from the EU. As a result, lenders will also be monitoring whether any change in law would render it unlawful for a lender to perform any of its obligations under the financing documents or fund or maintain its participation in the loan, triggering a mandatory pre-payment.

EIB investment has played an important role in the construction of offshore wind farms in the UK. Offshore wind projects in receipt of EIB funding include Beatrice, Galloper, West of Duddon Sands, Greater Gabbard, Sheringham Shoal, Thanet, London Array and Barrow.

Projects like these which are already funded will need to examine the terms of their credit agreements to establish the impact of Brexit. These contracts may include provisions requiring compliance with EU law, which exposes the offshore wind farm to the risk of regulatory mis-match to the extent that the UK and EU regulatory regimes diverge.

The more significant implications may be for projects which have not yet secured financing. In the short term, as an EU member state, the UK is still a shareholder of and contributor to EIB. In the longer term however, EIB funding will depend on the terms of the UK withdrawal settlement and the extent to which the investment opportunity furthers EU policy. EIB does invest outside of the EU and the EEA, investing for example in renewable energy projects in South Africa.

There is a possibility that the outcome of withdrawal negotiations results in some restrictions on the free-movement of people, goods and services between the EU and the UK. Depending on their nature, such restrictions may affect future offshore wind projects in the UK but might also impact operational projects, for example where technicians and components come from outside of the UK. Many operation and maintenance contracts and some EPC contracts contain “change in law” provisions that might be triggered as a result. Some such clauses refer to a change in law that affects the scope of the contractor’s services (so may not be affected by Brexit) but others just talk about causing the contractor additional cost (and so might be triggered).

Since the referendum vote, the Pound devalued dramatically against the Euro, making Euro denominated contracts more expensive for UK offshore wind. Where a project is incurring costs in Euros but is receiving revenue in Pounds, lenders will very likely have required the project to have hedged a proportion of that exposure at financial close for the term of the debt. The project’s exposure is therefore only in respect of any unhedged costs. This issue is particularly relevant to future projects where a significant proportion of supply and instalment contracts are likely to be denominated in Euros. A mitigant will be the extent to which those elements can be sourced from within the UK.

Consents for offshore wind farms between 1 and 100MW are granted pursuant to section 36 of the Electricity Act 1989 and those over 100MW pursuant to the Nationally Significant Infrastructure Project (NSIP) regime under the Planning Act 2008. ‘Development consent’ is the term given to consents granted under the NSIP regime. Both forms of consent are granted pursuant to domestic legislation and, as such, existing consents will not be affected by Brexit.

In respect of future applications for consent, the main potential impact may be to the requirement to undertake EU-derived Environmental Impact Assessments (EIAs). While international treaty obligations make it likely that the Government will seek to maintain a requirement for environmental assessments as part of the UK planning system, depending on the terms of the UK’s withdrawal from the EU, the Government may have scope to alter the assessment process to suit circumstances in the UK. This may result in fewer obligations on developers and planning authorities if the thresholds at which an EIA is required are increased. The Government may potentially review the ‘appropriate assessment’ regime required in respect of projects likely to have a significant effect on a European offshore marine site under the Habitats Directive 1992. This is discussed further below.

It is likely that once Brexit takes effect, the environmental standards applicable to offshore wind developments in the UK will change significantly. Of particular relevance is the Habitats Directive 1992 (as noted above) and the Birds Directive 2009 (the EU Nature Directives), which require that specified sites containing certain species and their habitats are conserved. The EU Nature Directives require offshore wind developments which are likely to have a significant effect on protected sites to undergo assessment procedures to determine any relevant safeguards that should be put in place. Offshore developers are also required to obtain marine wildlife licences before they can carry out activities that will impact species protected under the EU Nature Directives. It is likely that the EU Nature Directives will cease to apply to the UK once Brexit takes effect. This would be the case even if the UK joined the EEA in order to retain access to the single market, as the EU Nature Directives are excluded from the environmental legislation that EEA members must comply with.

As the EU Nature Directives have been implemented in the UK by domestic legislation such as the Offshore Marine Conservation (Natural Habitats) Regulations 2007, the Conservation of Habitats and Species Regulations 2010 and the Wildlife and Countryside Act 1981, once Brexit has taken place, Parliament may decide to water down or repeal them altogether. The Offshore Marine Conservation (Natural Habitats) Regulations 2007 and the Conservation of Habitats and Species Regulations 2010 have the ECA as their enabling legislation and so (similarly to the ROO), the Government will need to take some positive action to preserve this legislation upon withdrawal from the EU. The marine licensing regime under the Marine and Coastal Access Act 2009 (the MCAA) may also be impacted by Brexit, given that the MCAA was brought into effect partly to comply with the requirements of the Marine Spatial Planning Directive, the Marine Strategy Framework Directive 2008 and the Water Framework Directive 2008 with respect to the environmental quality of marine waters. It is important to emphasise that until Article 50 has been triggered and the ensuing 2 year negotiating period has expired, environmental legislation derived from European law will continue to apply.

Publication

The two-component tariff has been mandated in Vietnam pursuant to Article 50 of the amended Electricity Law 2024 and Government Decree 146/2025/ NĐ-CP.

Publication

Since the 2024 amendments to Ontario’s Construction Act under Schedule 4 of Bill 216 (Building Ontario For You Act (Budget Measures), 2024) received royal assent, project owners and construction companies have been holding their breath for the amendments to come into force.

Publication

The Sustainable Harnessing and Advancement of Nuclear Energy Act, 2025 (the SHANTI Act) came into effect in India on 21 December 2025. The SHANTI Act is the most sweeping reform of India’s nuclear regime to date, repealing the previously existing Atomic Energy Act, 1962 and the Civil Liability for Nuclear Damage Act, 2010 (CLND Act).

Subscribe and stay up to date with the latest legal news, information and events . . .

© Norton Rose Fulbright LLP 2026