New arguments appear for the first time in pleadings. If a financial institution only consults judgments in decided cases, it will not see over three-quarters of these arguments at all and the remainder only after about two years. By then, any litigation trend would be well-established. Accordingly, it is vital for risk management and strategic planning to be able to spot new arguments at the pleading stage.

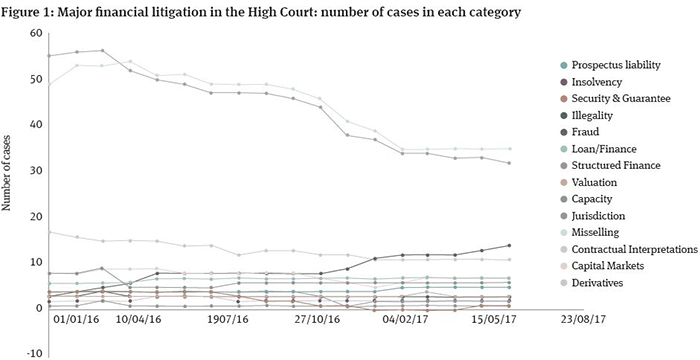

Using CID, Figure 1 sets out how many cases fall within a number of different categories, looking at major financial litigation in the High Court. Two trends appear. Firstly, there has been a marked decline in litigation relating to mis-selling and derivatives (and these two categories largely overlap).

This is undoubtedly due to time elapsed since the financial crisis. Abrupt dislocations in interest rates and other financial metrics during 2007 – 2009 led to litigation which, taking into account the six year limitation period and two year average case duration, is now winding down. This is a gradual process and new sources of mis-selling claims continue to arise, also generally related to market dislocations since the financial crisis. Nevertheless, it appears that the peak in derivatives mis-selling cases has passed – at least those based on interest rate hedging products sold to SMEs.

As set out above, the overall volume of cases has not seen a marked decline – so what is replacing derivatives mis-selling claims? All other categories of claim show little change, apart from one: fraud. There has been a steep increase in claims that involve allegations of fraud. A few years ago, there were typically two or three such cases involving banks being litigated at any one time. By the middle of 2017, there were 14 cases involving fraud. The lesson for banks and financial institutions is clear: they should be prepared to manage a greater number of fraud cases and they should understand the risk factors that lead to disputes involving fraud.

Why are there more cases alleging fraud?

The factual matrix underlying each particular dispute determines whether allegations of fraud are made and whether they are successful. However, it is possible to extract from recent and current cases various factors that might motivate allegations of fraud:

Circumventing basis clauses

“Basis clauses” are statements in a contract that set out the basis on which the parties are dealing, eg, a statement that a counterparty is a sophisticated investor. Courts have strictly enforced basis clauses, even where they effectively constitute exclusions of liability. They are not subject to the reasonableness limitations that apply to exclusion clauses as set out in the Unfair Contract Terms Act 1977 (UCTA). In fact, there have even been examples where the Court has held that a basis clause successfully precluded liability even where that clause would have been deemed unreasonable if UCTA had applied – see our previous articles on basis clauses, Contractual estoppel in mis-selling claims and Contractual estoppel and the duty to advise: Where are we now?.

An allegation of fraud is one way to revive a claim that is otherwise precluded by a basis clause. A party cannot rely on a basis clause to negate liability based on fraud. Accordingly, strict enforcement of basis clauses by the Courts over the last few years has created pressure which may have been relieved by increased pleading of fraud.

This suggests that fraud allegations arise where there has been a breakdown in the relationship between an investor and a financial institution and where the relationship between them was mediated by a contract that included a basis clause. This would include mis-selling claims as well as claims more widely involving bankclient relationships.

Obtaining new remedies

English courts have traditionally provided a wide range of remedies for fraud. In recent years, this has been further enhanced by their zeal to combat money laundering, bribery and corruption. Worldwide freezing orders, constructive trusts, equitable tracing and equitable receivership all form part of the flexible and effective tools available particularly in cases of fraud.

But the key remedial advantage when pleading fraud is the availability of rescission: the right to cancel the contract and put the parties in the position they were in before the contract was entered into. Where one party is seeking to extricate itself from a bad bargain, this is a tempting prospect.

Claims to rescind interest rate derivatives based on manipulation of LIBOR are an example. Interest rates moved unexpectedly following the financial crisis, leaving a number of businesses with hedging arrangements that were expensive and worthless. Basing a claim that would otherwise be simple mis-selling on fraudulent misrepresentation allows a party to cancel an unprofitable contract where no damages would be recoverable.

This suggests that fraud claims arise when banks or their counterparties are trapped in bad contracts, perhaps following abrupt market dislocations. For instance, they could be consumers alleging interest rate hedging products were mis-sold, or they could be securitisation issuers seeking to unwind one leg of back-to-back currency hedging arrangements. In all these cases, rescission is a powerful remedy, if fraud can be established.

Increased regulatory oversight

Since the financial crisis, banks have seen increased regulation and regulators have pursued wrongdoing with greater zeal. There have been several wide-ranging reviews of behaviour during and since the financial crisis, putting into the public domain voluminous detail relating to bank activity regarding LIBOR and other indices, interest rate hedges and many other products. Claimants may attempt to piggy-back on regulatory findings where they are investors in products that have been investigated by regulators or that refer directly or indirectly to indices that have been investigated by regulators. These claims are generally phrased in terms of fraud allegations.

Longer limitation periods

Claims involving fraud may be able to take advantage of longer limitation periods – in particular, where the claimant is not aware of the facts underlying the fraud until after the transaction is entered into. Given that the financial crisis occurred in 2008 – 2009 and that the standard limitation period is six years, many disputes are now in the critical stage immediately following expiry of the limitation period, when all claims other than based on fraud are barred.

This suggests that some of the fraud allegations may be motivated by an attempt to circumvent limitation periods and that this will naturally decline as we move beyond the critical period for most claims.

Will the trend continue?

Our analysis is inherently forwardlooking because we are examining current and ongoing litigation rather than decisions from completed cases. So the trends we identify here will start to be reflected in judgments in the next few years. In short, more judgments dealing with fraud will be a feature of English jurisprudence irrespective of whether the trend identified by CID continues.

Nevertheless, it is interesting to speculate as to whether new disputes will continue to allege fraud and whether the total volume of disputes before English courts will remain steady. Most of the drivers for fraud allegations listed above are still active. The political and business environment appears to have permanently embedded an increased focus on regulation and wrongdoing, so regulatory oversight and enhanced fraud remedies will continue to underpin fraud claims. Until the expansive view of basis clauses is changed – and many academic commentators think it should be changed – then this factor will also persist.

The only factor with waning influence is the extended limitation periods available for some fraud claims. Overall, then, fraud is likely to continue growing in importance. There may even be a positive feedback effect: when judgments featuring fraud arguments increase in frequency, this could inspire new claimants to include fraud arguments. In this way, a new higher level of fraud claims may become a visible feature of the litigation system.