On February 27, the Minister of Finance introduced the 2018 federal budget (Budget 2018), which proposed to implement the new excise duty framework for cannabis that was originally proposed in November 2017, to be effective when non-medical cannabis sales become legal in Canada. The excise duty will be imposed under the Excise Act, 2001 (Canada) and will apply to all cannabis products available for legal purchase (e.g., fresh/dried, oils and seeds and seedlings for home cultivation), including, somewhat controversially, medical cannabis products.

Cannabis cultivators and manufacturers will be required to obtain a licence from the Canada Revenue Agency (CRA) and remit the duty. Budget 2018 indicates that the CRA will begin accepting applications for cannabis licences and will issue excise stamps in advance of the legalization date. The excise duty will apply at the higher of two rates:

-

a flat rate based on the quantity of cannabis or seeds and seedlings contained in a product at the time of final packaging (i.e., when put in a container intended for sale to a final retail consumer); and

-

an ad valorem rate imposed at the time of delivery of a product to a purchaser (e.g., a provincially authorized distributor), which is in essence a percentage of the sales price of the product not counting the flat-rate duty.

The flat-rate duty will be calculated on a dollar-per-gram basis (or in the case of seeds/seedlings a dollar-per-seed/seedling basis) and will be higher on flowering material than on non-flowering material. The duty is payable by the licensee who packages the product for final retail sale and will be payable at the time of delivery of a cannabis product to a provincially authorized distributor.

All cannabis products that will be removed from the premises of a licensee and enter the retail marketplace must have an excise stamp with the applicable colour code for the provincial/territorial market they will be sold in. It will be the responsibility of the cannabis licensee who packaged the cannabis product to determine and apply the appropriate excise stamp before its entry into the duty-paid Canadian market. Products with THC concentrations of no more than 0.3% and cannabis-derived pharmaceutical products with a drug identification number and that are only available through prescription will not be subject to the duty.

Budget 2018 also proposes that goods and services tax/harmonized sales tax (GST/HST) will apply to cannabis products and seeds/seedlings and that the Excise Tax Act (Canada)will be amended to ensure cannabis products are not exempted or zero-rated under relieving sections related to basic groceries or agricultural products.

Pursuant to an agreement reached between the federal government and participating provinces and territories in December 2017 on a coordinated cannabis taxation framework for the initial two years after legalization, 75% of the taxation revenues from a combined $1 per gram / 10% excise duty rate will flow to participating provinces and territories, with the federal government receiving the remaining 25%. Currently Manitoba is the only non-participating province or territory. The federal portion of cannabis excise duty revenues will be capped at $100 million annually for the first two years after legalization, with any additional cannabis excise duty revenues being distributed to the participating provinces and territories.

The agreement also provides for the application of an additional excise duty in respect of provinces and territories that agree to participate in the coordinated framework and will apply on the same tax base as, and in fixed proportion to, the federal rate. It will also be possible for a province to ask for an adjustment to the additional excise duty to reflect differences between the sales tax rate applicable to cannabis in the province and the highest prevailing general sales tax rate, or rate of the provincial component of the HST, among provinces. The proposals contained in Budget 2018 are generally consistent with the December 2017 agreement.

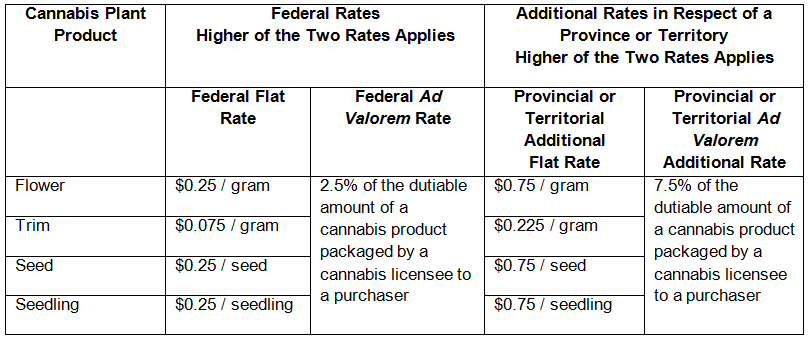

The following table summarizes the proposed combined federal and provincial or territorial excise duty rates for cannabis products:

Budget 2018 announced that the excise duty framework for cannabis taxation is proposed to be in place by the time cannabis for non-medical purposes becomes accessible for legal retail sale. Duty will become payable for cannabis licensees on any cannabis products they have already delivered in advance of the legalization date for eventual retail sale. On or after the date of cannabis legalization for non-medical purposes, all cannabis products delivered through the mail in accordance with the Cannabis Act (Canada) will be subject to the appropriate duty.