Publication

The new framework for stopping scams before they start

Scams are a global phenomenon and no business is immune. In addition to reputational damage and a likely increase in customer complaints.

Ten things to know

Global | Publication | March 2016

Greece enjoys a remarkable wind resource with local average wind speeds (at hub height) often exceeding the 8–10 m/s, especially in the Aegean Sea islands and on mountain ridges on the mainland. Its 2020 national targets for renewables currently translate, for wind power alone, into at least another 2GW of installed capacity.

However, due to the current economic climate in Greece, investors reasonably call for strong policy commitment, the emergence of a stable economic environment and for a favourable support scheme for renewables to remain in place. These are required to maintain investor confidence in the Greek wind power sector which continues to deliver considerable returns on investment despite the change in feed-in tariffs in April 2014.

This publication gives an overview of the wind power sector in Greece, with a particular focus on the key issues for investors and the prospects for future wind power projects in the country.

In spite of the licensing and development hurdles faced by project developers, Greece has made substantial progress in promoting and supporting renewables. Having commissioned the first commercial wind park in Europe (built in 1983 on the Cycladic island of Kythnos), in 2015 Greece exceeded 2,150MW of installed wind power capacity, which produced 4.6TWh at a weighted average price of €89.4 per MWh.

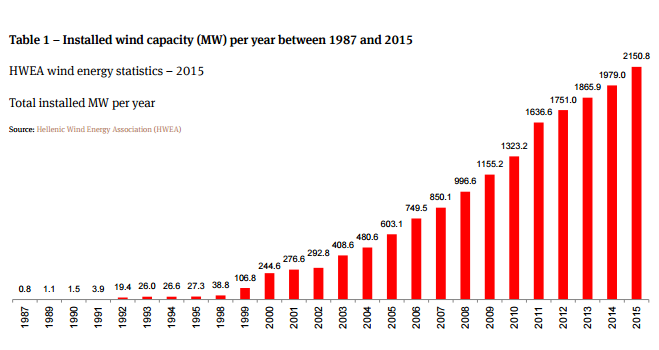

Table 1 – Installed wind capacity (MW) per year between 1987 and 2015

HWEA wind energy statistics - 2015

Total installed MW per year

Source: Hellenic Wind Energy Association (HWEA)

In the last ten years Greece experienced a fourfold increase in installed wind capacity. In 2015, the total installed capacity of renewables exceeded 5.2GW (out of a total installed capacity of circa 20GW, including 2.6GW of photovoltaic (PV) capacity) and produced 10.7TWh.

This demonstrates the shift in national energy policy from overdependence on indigenous lignite (with 4.5GW installed capacity and 20.3TWh of electricity produced in 2015) to renewables in addition to existing large hydro power plants (totalling circa 3.2GW).

Despite this, the national 2020 targets for renewables under the Renewables Directive1 are ambitious including 20 per cent of gross final energy consumption; 20 per cent of heating and cooling power; and 40 per cent of gross electricity production coming from renewable energy sources by that year. Although these targets are yet to be achieved, in 2015 more than 15 per cent of gross final energy consumption and around 25 per cent of gross electricity production came from renewables, including large hydro power plants, although the official figures for 2015 are expected in May 2016. In light of these targets, the 2010 National Renewable Energy Action Plan envisaged 7.5GW of wind power capacity by 2020 although more recent calculations estimate the additionally required renewables capacity at around 2.5GW. However, there is still significant potential for growth of the Greek wind power sector to achieve the 2020 national targets and beyond, with increasing interconnection with the Aegean Sea islands and Crete facilitating this.

In June 2015, the Greek wind power sector had almost half a dozen large, first tier market players with operating wind parks exceeding 100MW and a considerable pipeline of projects. The first tier includes the Athens Exchange (ATHEX) listed renewables subsidiaries of two major construction groups; Terna Energy of GEK Terna Group (369.6MW) and Eltech Anemos of Ellactor Group (199MW). The first tier also includes renewables subsidiaries of three major European utilities; EDF EN Hellas (358MW); Iberdrola Renovables (250.7MW); and Enel Green Power (200.5MW). Together they account for almost 1.4GW of a total of 2.08GW installed capacity.

The second tier includes domestic players like PPC Renewables of Public Power Corporation (PPC); RF Energy; Eunice; and Protergia of Mytilineos Group, and overseas investors like Acciona; Babcock & Brown; and Reninvest, all together totaling around 362MW of wind power capacity. A further circa 260MW of wind power capacity is held by another dozen much smaller players, each with more than 10MW. This indicates the consolidation of the Greek wind power sector primarily in the hands of experienced market players.

In the mid-1990s, a special support scheme for renewables was introduced as an incentive for independent power production in Greece. There were two elements to this support scheme; one was a renewable energy purchase obligation placed on the network operator and the other was a regulated feed-in tariff for the purchase of such energy. At the same time additional subsidies were also available for renewable energy projects in the form of either cash grants or equipment leasing subsidies or income tax exemptions as an investment incentive in compliance with EU State aid law and with different subsidy ceilings depending on the location of the project.

In parallel with the liberalisation of the electricity market and in compliance with the first2 and the second3 EU Electricity Directives, a special law on renewables was also enacted in 2006 and later enhanced in 2010 in full transposition of the Renewables Directive(s)4. This resulted in the current support scheme for wind power in Greece (see further below) and accelerated the development of all renewables, including wind power projects.

The implementation of these measures led to €2.6 billion of investment in the wind power sector. Despite this, an additional investment of the same size is required in order for Greece to meet its 2020 national targets for renewables, including required grid infrastructure expansions.

Power Purchase Agreements (PPA)

Subject to grid safety and technical limitations, renewable energy power plants such as wind parks are entitled to priority dispatch of their power output. This means that the off-taker is legally obliged to off-take wind power at regulated feed-in tariffs and the competent grid and market operators must ensure that the off-take takes priority over electricity produced from conventional energy sources. Priority dispatch is given by the competent grid operator pursuant to the relevant grid code and the relevant standardised (regulated) PPA. The PPA is entered into between the wind power producer and (a) the Energy Market Operator (or LAGIE by its Greek abbreviation) for wind projects in the Interconnected System of Greece (which basically covers mainland Greece) or (b) the Distribution Network Operator (or DEDDIE by its Greek abbreviation) for wind power projects in the non‑interconnected islands of Greece. An independent transmission operator (or ADMIE by its Greek abbreviation) is responsible for transmission system operations in the Interconnected System. The PPA is for a term of 20 years from the date of the wind park’s operation licence.

Additional subsidies currently available

Since January 1, 2014 cash grants and equipment leasing subsidies are no longer available for wind projects, except for hybrid wind/water pumped-storage projects that can still benefit from cash grants under the current investment incentives programme. Income tax exemptions for the creation of tax-free reserves have recently become the sole additional subsidy available for conventional wind projects whether onshore or offshore. However, in practice, project sponsors traditionally opt for the higher feed-in tariffs instead of these tax exemptions (see further below).

Feed-in tariffs (FiT) including FiT uplift for offshore wind

The level of the feed-in tariffs for wind power projects depends on installed capacity, location of the project and whether or not the project has received any other subsidy. Since April 7, 2014 the feed-in tariffs for new wind power projects, which are connected to the grid after that date, are the following:

Table 2 – Feed-in Tariffs (FiT) for new wind power projects after April 2014

| Type of wind power project | FiT (€/MWh) | |

|---|---|---|

| w/out subsidies | with subsidies | |

| Onshore wind power projects ≤ 5 MW | 105 | 85 |

| Onshore wind power projects > 5 MW | 105 | 82 |

| Onshore wind power projects in the Non-Interconnected Islands | 110 | 90 |

| Offshore wind power projects | 108.30* | |

* The feed-in tariff (FiT) for offshore wind parks may be increased by up to 30% based on substantiated investment costs.

FiT uplift for dedicated subsea cables

Wind parks built on non-interconnected islands and uninhabited islets that are connected to the mainland system through dedicated submarine cables (paid for entirely by the project sponsors) are entitled to a feed-in tariff uplift of up to 25%, depending on the particular cable’s length. This will be the case for the first wind park in Greece which will be built on an uninhabited islet near Attica that is currently under construction by Terna Energy. It is expected to come into operation by mid-2016 with a total 73.2MW installed capacity. Similar islets and islands locations are also under consideration by several project sponsors in Greece given the excellent wind potential identified in these locations.

Wind power producers are also entitled to additional compensation at the end of each calendar year for up to 30 per cent of any output curtailments imposed for reasons of grid stability and safety. This ceiling may increase annually up to 100 per cent so that the total additional compensation for any output curtailments is equal to the lower of:

As in other European countries, the initial feed-in tariffs and the additional subsidies previously available for PV power resulted in an unprecedented fivefold expansion of PV capacity to 2.6GW between 2010 and 2013. This ‘solar boom’ together with some inherent inefficiencies of the domestic energy market created a significant deficit in the Special Account for Renewables managed by LAGIE for purchasing renewable energy under PPAs.

The government and the Regulatory Authority for Energy (RAE) took a series of measures between 2012 and 2014 to restore liquidity in this special account, which is largely funded by final consumers through their electricity bills. Although drastic, these measures (e.g. successive downwards revisions of feed-in tariffs for PV projects, suspension of PV licensing, successive increases in the renewables duty paid by final consumers, special solidarity levy on renewable power producers, additional sources of revenues for the special account) did not deliver in full and in March 2014 the aggregate deficit amounted to €0.5 billion.

The April 2014 ‘new deal’ and its effect on operating wind parks

A ‘new deal’ was therefore required and was reached after long consultation with stakeholders. The April 2014 ‘new deal’ for renewables was implemented in the wind power sector through:

At the same time, the special solidarity levy was repealed for all renewable power producers.

Table 3 - Feed-in Tariffs (FiT) in €/MWH for operating wind parks after April 2014

| Grid connection timing | Interconnected System | Non-Interconnected Islands | ||||||

|---|---|---|---|---|---|---|---|---|

| ≤ 5 MW | > 5 MW | ≤ 5 MW | > 5 MW | |||||

| w/out | with | w/out | with | w/out | with | w/out | with | |

| until 31/12/2006 | 107 | 87 | 107 | 84 | 120 | 93 | 120 | 90 |

| from 01/01/2007 | 107 | 89 | 107 | 86 | 120 | 95 | 120 | 92 |

Additionally subsidised wind parks (indicated above as ‘with’) appear to have suffered a greater haircut than non‑subsidised ones (indicated above as ‘w/out’) taking also into account the annual adjustment for inflation applied in the past to the previously applicable feed-in tariffs. According to market reports, even after the above haircut, the average internal rate of return (IRR) for islands-based wind parks is approximately 19 per cent and around 14 per cent for mainland-based ones, while new wind parks in the mainland are expected to achieve between 10 per cent and 15 per cent IRR under the current support scheme for renewables.

Hence, there are no obvious signs of financial distress for operating wind parks in Greece and their IRRs appear reasonable even after the ‘new deal’ of April 2014. The deficit in the Special Account for Renewables has also been considerably reduced during 2015. At the end of 2015 the Special Account for Renewables had an aggregate deficit of only €82.6 million compared to the €0.5 billion deficit of March 2014.

In April 2014 the European Commission adopted new Guidelines on State aid for environmental protection and energy for 2014–2020, which came into force on July 1, 2014. These Guidelines replaced the 2008 guidelines on aid for environmental protection, and are applicable until the end of 2020. The new Guidelines are intended to assist the EU Member States to design State aid schemes that help them reach their climate change and energy sustainability targets without threatening to distort competition in, or otherwise fragment, the EU market. For more on these Guidelines please read our briefing on ten things to know about the new EU guidance on State funding in the energy sector.

The new Guidelines aim to better integrate renewables into the internal electricity market in a gradual way, introducing competition between different technologies. Feed-in tariffs will be progressively replaced by competitive bidding. During 2015–2016, Member States are expected to start implementing competitive bidding procedures for a small proportion of their new capacity from renewables. From 2017, operating aid to new renewable energy installations should, in principle, be granted through a competitive bidding process. The new Guidelines will have no effect on State aid paid to the owners of existing installations. These owners will continue to receive State aid based on existing approved State aid schemes in order to maintain investors’ legitimate expectations on the returns on their existing investments.

However, the current feed-in tariff support scheme for the provision of operating aid to wind power in Greece (described above) is no longer available to new wind parks entering into the relevant PPA after December 31, 2015 . Instead, a market-based support scheme will be introduced for such new wind parks, especially in the Interconnected System of Greece. Non-interconnected islands may be excluded from the new market-based support scheme for currently lacking wholesale electricity market structures and until they are interconnected. A proposal for this new support scheme covering the period 2016–2020 was submitted for public consultation by the Ministry of Environment & Energy in late February 2016. The new support scheme will have to be approved by the European Commission before it is enacted.

According to the proposed scheme, new wind parks in the Interconnected System of Greece with more than 3MW installed capacity and a PPA dated after December 31, 2015 will be entitled to a feed-in premium (FiP) on top of their power sales revenues from the Greek wholesale electricity market (where they will be participating through zero-priced electricity offers in order to maintain their priority dispatch status) and up to a maximum reference price (currently set at €98 per MWh) for a term of 20 years. The reference price(s) (per renewable energy technology) will be set annually and will take into account the levelised cost of electricity (LCOE) generation from renewables, financing and equity costs for renewables. Revised reference prices will be published two calendar years before they become applicable. In addition, from January 1, 2017, competitive bidding procedures will be introduced for new power capacity from renewable energy sources provided that this does not lead to suboptimal results described in the new Guidelines. Although the proposal does not elaborate, it is reasonably expected that such a competitive bidding will result in the applicable reference price for the project concerned.

For more on the proposed scheme please see our recent briefing on the proposed new support scheme for renewable electricity in Greece.

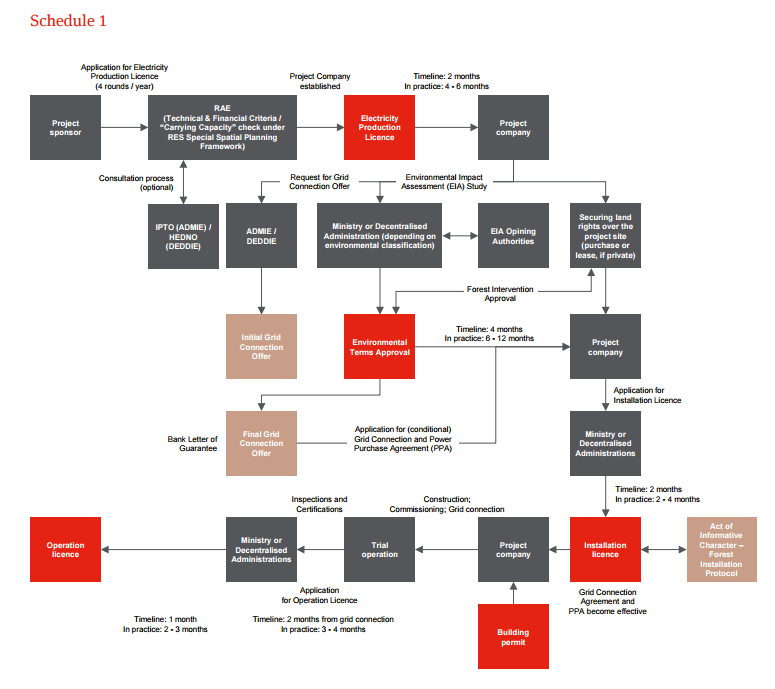

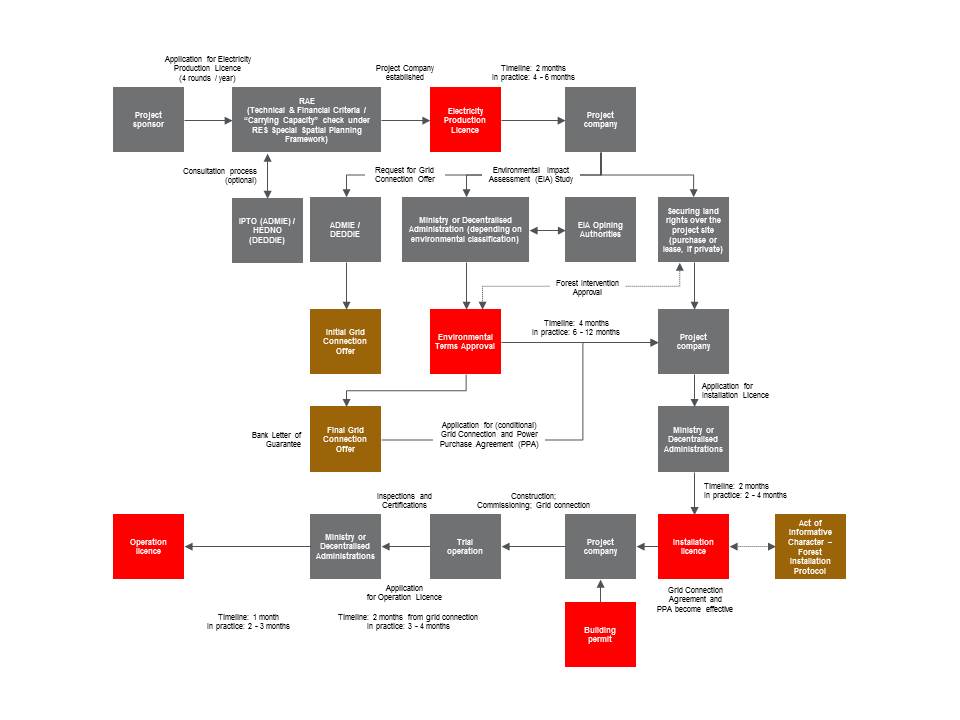

In Greece the licensing, development, construction, commissioning and operation of any type of renewable or conventional energy power plant is heavily regulated. In this context there are five main licences that a utility scale wind park (i.e. ≥50kW) is required to obtain for its lawful development, construction and operation under the authorisation model adopted by Greece for new renewable energy capacity. These are the following and they are obtained in the following order:

Because of the significant classical antiquities and the Byzantine monuments found in Greece as well as the various Natura 2000 areas around the country, the environmental licensing of a wind power project is the most critical licensing stage in its development. The Special Spatial Planning Framework for Renewables of December 2008 and an extensively revised framework on the environmental licensing of projects in Greece, which was adopted in September 2011, have removed a lot of uncertainty and ‘red tape’ surrounding the spatial planning and the environmental licensing of wind power projects in Greece.

Except for the Environmental Terms Approval and the Electricity Production Licence, where the environmental licensing authorities and RAE perform a substantial review of the proposed wind power project, the remaining main licenses are more of a formality with checks by the relevant authorities of the prerequisites and properly documented project-specific information required by law to be submitted by the project sponsor, subject to successful testing where required.

A flowchart of the licensing process for wind projects in Greece is included as Schedule 1.

Wind and other renewable power producers are entitled to non-discriminatory and transparent grid access based on their third party access right to a regulated natural monopoly such as the grid (either the distribution network or the transmission system) in accordance with the EU Electricity Directives and the relevant national laws and regulations (for example, the System Operation Code).

In practice, grid access for renewable energy projects of up to 8MW is secured through the Distribution Network Operator (or DEDDIE by its Greek acronym). For projects in excess of 8MW, it is secured through the Independent Power Transmission Operator (or ADMIE by its Greek acronym).

The relevant grid operator elaborates on the required grid connection works and their estimated cost for the producer through an indicative budget. Shared grid connection works are often required by the grid operator regardless of a joint application for grid access.

Once a wind power project receives Environmental Terms Approval, the initial grid connection offer becomes final and binding on the relevant grid operator for a term of three years, provided that it is timely accepted in writing by the project company. The three year term may be extended for the term of the Installation Licence, including any extensions.

The extension of the term of the Installation Licence has often proven controversial because if the Installation Licence lapses without the project commencing trial operation, this suggests that the project is not feasible. It would also enable the revocation of the project’s Electricity Production Licence and freeing up grid capacity for competing projects, especially in windy areas with limited grid capacitySince 2015, all renewable energy project sponsors with final grid connection offers in place are required to demonstrate their commitment to grid connection by submitting to the competent grid operator security for the connection in the form of bank letters of guarantee. The letters of guarantee must be for a term of at least two years and remain in place until the timely grid connection and start of trial operation of the projects concerned. Failing to meet these requirements would mean a grid connection offer lapses. The amount of this guarantee is calculated per MW of nominal capacity of each project and can be quite high for portfolios of wind projects. However, once the relevant standard form Grid Connection Agreement has been executed, the amount of the guarantee is reduced to one quarter of the original amount.

The vast majority of existing wind parks in Greece with an installed capacity in excess of 10MW are located in south mainland Greece, south Evia, Peloponnesus and Thrace. Despite their wind potential, the rest of mainland Greece, as well as the Aegean Islands and Crete, are yet to be exploited. This is due to limited grid capacity and the lack of adequate interconnection with mainland Greece where most electricity demand is located. Wind power projects in mainland Greece often depend on grid reinforcements and extensions at the cost and initiative of the interested project sponsors. However, unlocking the great wind potential of the Greek islands depends on some critical interconnections, some of which are expected in the short to medium term, with the exception of Crete which is a long term infrastructure project.

The recent completion of a new 150kV submarine interconnection between south Evia island and Attica region will enable the development of 380MW of new wind power capacity in south Evia and the nearby Cycladic Islands of Andros and Tinos. The development has an estimated investment value of €700 million which will be sponsored by some of the prominent market players.

However, the project sponsors face an imminent additional cost allocation of €150,000 per MW of licensed capacity to pay for the interconnection. This additional cost, combined with limited funding currently available for many project sponsors, will most likely lead to acquisition opportunities for a number of wind power projects at an advanced stage licensing wise. These projects may prove attractive, being located in a very windy area which, together with central Greece, is one of the most promising Wind Priority Area(s) for development of 3,240MW mandated under the 2008 Special Spatial Planning Framework for Renewables. Moreover, the scheduled upgrade of existing grid infrastructure in the area to 400kV will enable the development of additional 450MW– 550MW of wind power capacity in south Evia in the future.

The ongoing interconnection of some major Cycladic Islands with Cape Lavrio in Attica region, which is scheduled to be completed by the end of 2016, will enable the development of another 200MW–250MW of new wind power capacity in another very windy area of Greece with offshore wind features that are practically untapped to date. However, local communities that are heavily involved in the tourism industry are not particularly keen to accommodate wind parks on their islands despite the environmentally friendly profile that wind parks can provide to those communities as a competitive advantage over other neighbouring tourist destinations.

ADMIE, the system operator, has included the interconnection of Crete with mainland Greece in Attica and/or Peloponnesus in its ten-year system development programme for 2014–2023. Three optional scenarios are examined in order for such an ambitious project to materialise by 2020. 800MW of new wind power capacity could be installed in Crete in the base case scenario of an interconnection with Peloponnesus (expanding to 1,200MW and reaching 1,600MW in the more ambitious scenarios of a direct interconnection with Attica).

In this context there are major players who are developing large clusters of wind power projects in Crete, including an innovative hybrid project comprising water pumping/ storage (100MW) and wind power of 90MW installed wind capacity and 75MW guaranteed output capacity. This project is expected to enjoy special feed-in tariffs available to hybrid renewable energy projects under the applicable legislation.

However, the estimated €850 million to €1 billion budget required for such an interconnection project makes it quite challenging under the current economic conditions. Alternative means of funding are proposed by stakeholders such as project bonds and public-private partnerships. This would enable the implementation of this ambitious interconnection project that is required, not only for renewables and wind power exploitation on the island, but also for grid stability purposes and to minimise black-outs risk in a popular tourist destination like Crete.

Since 2012, Peloponnesus, a Wind Priority Area for 875MW (in its South-East tip only) under the 2008 Special Spatial Planning Framework for Renewables, has officially been declared as a grid congested area with a maximum of future wind capacity estimated at 1,100MW out of 1,900MW in total for renewables. Following completion of the ongoing upgrade of Peloponnesus’ grid infrastructure to 400kV, it is expected that up to 2,200MW of wind power capacity could be safely installed in Peloponnesus, including 475MW of existing operational wind parks. Subject to any spatial planning and environmental limitations, 1,700MW of new wind capacity could be installed in the area in the medium term.

Thrace, also a Wind Priority Area for 960MW under the 2008 Special Spatial Planning Framework for Renewables, is yet to be declared as a grid congested area. However, in practice, the delayed completion of certain grid upgrade and expansion works in the area means that new wind power capacity cannot currently be developed. Upon completion of these works an additional 700MW–900MW of new wind power capacity could be added to the existing 245MW of operating wind parks in Thrace.

Greece has a total coastline of more than 20,000km, including uninhabited islands and rocky islets which make up approximately 3,000km. Such a sea frontage combined with an excellent wind potential should not be disregarded as far as offshore wind energy is concerned. However, the various limitations, including but not limited to the availability of onshore sites with similar wind potential; the steep sea-bed drop-off around mainland Greece and around the Aegean Islands; offshore wind technology costs; and military and environmental restrictions have made offshore wind a challenging quest in the Aegean Sea.

Despite these limitations, a number of offshore wind power projects are being promoted by various project sponsors but only two of them have managed to obtain an Electricity Production Licence from RAE so far: offshore Alexandroupolis in Thrace for 216MW; and offshore Limnos Island in the northern part of the Aegean Sea for 498MW. A special review of proposed offshore wind projects is required by law as regards their energy efficiency and economic feasibility. The proposed grid connection option is also critical for offshore wind power projects.

Since November 2011, no new applications for offshore wind power projects have been possible. Instead, a central licensing scheme is provided for by law whereby offshore wind concessions, including a grid connection option, are to be offered by the State to interested investors through a bidding process after a Strategic Environmental Assessment is performed by the State. It is unlikely that the State will initiate any such tender shortly. In any event, the financing of offshore wind projects in Greece may prove difficult under the current economic conditions, given offshore wind technology costs and the currently applicable feed-in tariff notwithstanding the conditional 30 per cent maximum uplift for substantiated investment costs (see Table 2). Further, the feed-in premium (FiP) support scheme through competitive bidding procedures (briefly described above) is also envisaged to apply also to offshore wind power projects after December 31, 2015 in accordance with the European Commission’s new Guidelines on State aid for environmental protection and energy for 2014–2020.

Bond loans issued under the Greek Bond Law 3156/2003 (also known as Securitisation Law) in conjunction with Codified Law 2190/1920 on Sociétés Anonymes (companies limited by shares) are the most common financing structures used for wind power and other infrastructure project finance in Greece. This is not only because of the favourable treatment on security costs and tax issues, but also because of the novel and efficient way that security can be given to groups of creditors – bondholders (at least two are typically required) and the structure of the bonds in the name of the bondholder agent (who essentially acts as the security agent of the creditors).

Four types of bond loans are possible for Greek sociétés anonymes, which is the preferred type of wind project company vehicle for private investors: common bond loans; exchangeable bond loans; convertible bond loans; and bond loans with a right to participate in the profits of the issuer – borrower. Common bond loans are generally the first choice for credit institutions such as banks.

Full project finance security is typically granted under a bond loan including: a pledge over the shares of the issuer; pledge over receivables under the PPA and other receivables of the issuer, as well as over claims under insurance policies of the project; pledge over the bank accounts of the issuer; non-possessory pledge over the equipment of the project; and direct agreements with major project parties like an Engineering, Procurement and Construction (EPC) contractor and the turbine supplier. Simplified perfection and enforcement procedures are also applicable to such security pursuant to special laws, including appropriation of listed pledged shares and arguably also non-listed ones pursuant to financial collateral arrangements under Greek law.

One key issue for private investors and financiers of renewables and wind power projects in Greece is change in law risk. The applicable feed-in tariff is linked to the law rather than to a contract in the sense that the PPA does not provide for a specified feed-in tariff as a numerical price in Euros per MWh for the term of the PPA. It is therefore more susceptible to legislative intervention. Until April 2014 feed-in tariffs for wind power and other renewables were adjusted only for inflation. Since April 2014 all feed-in tariffs may be revised, apparently downwards, by decision of the competent minister following an opinion from RAE depending on national energy planning and needs, renewables penetration into national energy balance, achievement of national targets for renewables and declining technology costs. The same provision of law, however, provides for grandfathering whereby any such decision will only apply to renewable and wind power projects that connect to the grid after two calendar years from the end of the calendar year during which such a decision is adopted. This should result in adequate lead times for any new projects falling under the current support scheme for renewables to be commissioned and to remain entitled to the current feed-in tariffs.

The pending introduction of a market-based support scheme for renewables in accordance with the new Guidelines of the European Commission on State aid for environmental protection and energy for 2014–2020 constitutes the major legal and commercial issue for new wind power projects, project sponsors and financiers, in relation to medium to long term investment plans and wind project financings in Greece. As discussed above, feed-in premiums (FiPs) are proposed by the Greek state as the optimum market-based support scheme for wind power and other renewables in Greece for the period 2016-2020. FiPs will provide revenues on top of wholesale electricity market revenues but subject to a ceiling reference price, which will be initially set administratively but which will then derive from a competitive bidding process from 2017. For more on the proposed scheme please see our recent briefing on the proposed new support scheme for renewable electricity in Greece.

The Energy Union Package put forward by the European Commission in February 2015 and approved by the European Council of Ministers in March 2015 will also be relevant for the promotion and support of renewables, not only in Greece but also across EU Member States. For further details, please refer to our relevant portal and briefings.

Another key issue for private investors and non-EU financiers is that the project revenues and any other receivables under the PPA are typically assignable only to EU-established and Greek banks. Non-EU banks, equity or pension funds, or other financiers, must receive prior written consent of LAGIE or DEDDIE, as the case may be, in their capacity as the off-takers under the relevant PPA. Without this consent, the assignment is void and is not binding on the off-taker, instead giving it a right of suspension and termination of the PPA. Hence, the security available to financiers from third countries is at the discretion of the off-taker which – to the best of our knowledge – has not been tested in practice yet. However, it should not be an issue for non-EU financiers that can demonstrate their financial credibility

Directive 2009/28/EC of the European Parliament and of the Council of 23 April 2009 on the promotion of the use of energy from renewable sources and amending and subsequently repealing Directives 2001/77/EC and 2003/30/EC

Directive 96/92/EC of the European Parliament and of the Council of 19 December 1996 concerning common rules for the internal market in electricity

Directive 2003/54/EC of the European Parliament and of the Council of 26 June 2003 concerning common rules for the internal market in electricity and repealing Directive 96/92/EC

See above footnote 1.

Publication

Scams are a global phenomenon and no business is immune. In addition to reputational damage and a likely increase in customer complaints.

Subscribe and stay up to date with the latest legal news, information and events . . .

© Norton Rose Fulbright LLP 2023

{kind=link}