Reported Baseline Calculation

The reported baseline for large facilities will be calculated by the Clean Energy Regulator (Regulator) and as mentioned will be based on your reported NGERs data for the five year period between 2009/10 and 2013/14. The Regulator will initiate the reported baseline setting process by advising responsible emitters of their proposed facility baseline number. The Regulator aims to contact all responsible emitters with their proposed reported baselines by May 2016.

If you satisfy the reported baseline criteria and believe that your projected emissions into the foreseeable future will remain below your highest reported scope 1 emissions value from 2009/10 to 2013/2014, then no further action regarding baselines is likely to be required. You should not trigger the historic baseline and will not be required to purchase ACCUs.

Optional Reported Baseline for Some Facilities

Facilities that only reported scope 1 emissions under NGERs in some of the 5 years from 2009/10-2013/14 may have a choice to opt-in to receive a reported baseline number. If you have reported scope 1 emissions under NGERs four or less times in the five years from 2009 and have only reached the threshold of more than 100,000 tonnes covered emissions in one to three of those years, you can either:

- Request a reported baseline determination, which requires you to notify the Regulator by July 31, 2016; or

- Use the calculated baseline approach under the new facility criteria, which requires you to submit an application by October 31, 2017 along with an independent audit report.

If you are in this position and don’t follow options 1 or 2 above, the Regulator will give you a default baseline number of 100,000.

For a reported baseline determination, the Regulator will provide you with feedback regarding the proposed baseline and provide opportunity for comment / consultation before the actual determination is made. Once a reported baseline determination is issued for your facility, it will no longer meet the new facility criteria for a calculated baseline.

Calculated Baselines

If you expect your facility’s baseline emissions to exceed your reported baseline, then it is recommended that you consider applying for a ‘new’ baseline under the calculated baseline criteria. This is your ‘free-kick’!

For a calculated baseline that begins from July 1, 2016, applications can be submitted between July 1, 2016 and October 31, 2017. The baseline is determined by the highest expected production level (and corresponding emissions) over the three-year period covered by the calculated baseline determination (2016/17 to 2018/19 for a baseline determination starting July 1, 2016). However, the years you can choose from to set your baseline are limited by the date from which you apply:

- to use the highest production level from all three years to determine your baseline, you need to submit your application by July 30, 2016; otherwise

- if you submit your application by July 30, 2017, you can use the highest of the last two years (2017/18; 2018/19) to determine your baseline number; alternately

- if you submit your application after July 30, 2017 and by October 31, 2017, your emissions baseline number will be established from your production level in 2018/19 only.

Because these application dates are not straight forward, we have provided a practical case study further below to illustrate when applications need to be submitted. You can also see Ndevr Environmental’s recent article on key dates for calculated baseline applications here. It is important to understand forecast emissions early to make an informed decision about when to submit your application, accompanied by an audit report.

The calculated baseline provides an opportunity for facilities to ‘adjust upwards’ their baseline, if it is reasonably expected that the facility’s emissions will increase. The specified criteria to be eligible for the calculated baseline include:

- increase or expected increase of baseline emissions within the first year 2016-17 of the Safeguard Mechanism (initial baseline criteria)

- new facilities that forecast expected emissions of 100 000 t CO2-e in the first year of the calculated baseline (new facility criteria)

- facilities in the natural resource sector that have variable emissions due to resource extraction or the quality of the grade ore (inherent emissions variability criteria)

- when facilities expect their baseline to be permanently increased if there is a production capacity growth greater than 20% (significant expansion criteria).

If you think your facility will satisfy one or more of the calculated baseline criteria, then you can apply to the Regulator for a calculated baseline. Generally, the calculated baseline is determined by the following calculation:

Calculated baseline = forecast production x forecast emissions intensity

Because the initial calculated baseline option is likely to be of interest to industry, and important dates are approaching, we have prepared an abridged case-study to demonstrate how a company might apply for an ‘initial calculated baseline’.

Case Study

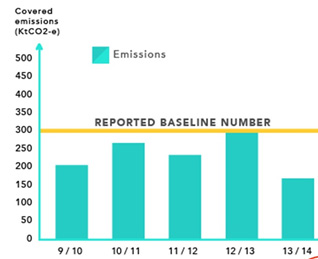

You have operational control of Facility ‘X’. Based on the past emissions for Facility ‘X’ in Figure 1 below, the reported baseline will be 300,000 t CO2-e.

Figure 1. Past Emissions Profile

Source: Ndevr Environmental Consulting (18 April 2016)

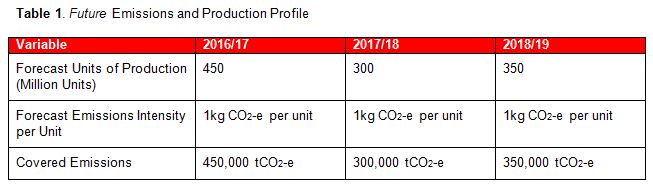

Based on your projected future emissions in Table 1 below, you think you will exceed this (reported) baseline as soon as the Safeguard Mechanism starts.

What can you do?

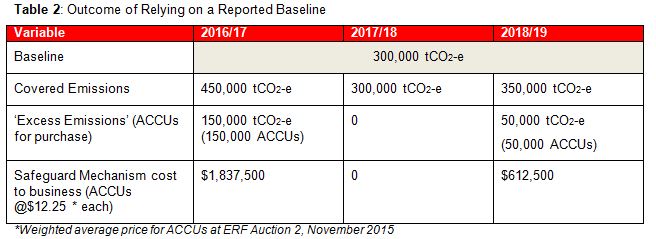

In this scenario, if the facility was to rely on a historic ‘reported’ baseline (300,000 tCO2-e from the 2012/13 year) it would be subject to the costs demonstrated in Table 2.

For Facility ‘X’, assuming it can source ACCUs at $12.25 each over the next three years (equal to the weighted average price paid by the Government at ERF Auction 2), the direct cost to business over the three years is $2,450,000.

In this instance Facility ‘X’ should look to apply for an initial calculated baseline.

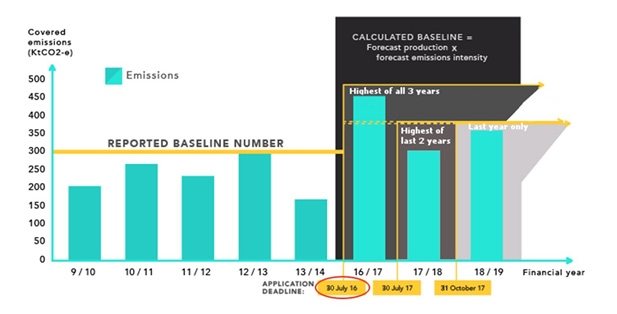

Under Figure 2, Facility ‘X’ should establish its baseline number based on forecast production levels from 2016/17, which will present the highest covered emissions during the three year calculated baseline determination period.

Figure 2. Past Emissions and Application dates for calucated baseline determation beginning July 1, 2016

Source: Ndevr Environmental Consulting (18 April 2016)

Using the forecast production and emissions intensity from Table 1, the calculated baseline would be as follows:

Calculated baseline

= forecast production x forecast emissions intensity

= 450M units x 1kg CO2-e per unit

= 450,000 tCO2-e

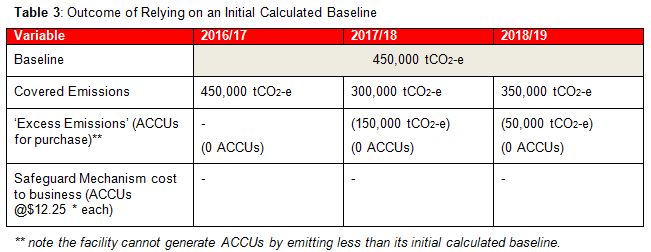

With an initial calculated baseline in place, Facility ‘X’ would have no cost to business, other than compliance costs associated with auditing and developing the initial calculated baseline demonstrated in Table 3.

In this simplified case study, Facility ‘X’ is in a much better position by utilising an initial calculated baseline. Excluding the costs of auditing and developing the initial calculated baseline, the facility is $2,450,000 in front.

Importantly, as per Figure 2, because Facility ‘X’ wants to establish its baseline number on forecast emissions from the 2016/17 year, which will present the highest covered emissions during the three year calculated baseline determination period, it must submit its application and audit report by July 30, 2016.

If the application is submitted after July 30, 2016 and by July 30, 2017, then the baseline number for the three year period will be based on only the last two years of forecast emissions, which in this case is 350,000 tCO2-e (in 2018/19). For Facility ‘X’, because projected emissions in year 3 of the baseline determination period are higher than in year 2, the baseline number will be the same if the application is submitted after July 30, 2017 but before and by the final deadline of October 31, 2017 (and therefore based on the final year only).

Here, even after taking advantage of a three multi-year monitoring period which allows Facility ‘X’ to take the average emissions across the three years (366,666 tCO2-e), Facility ‘X’ will still need to offset 50,000 t CO2-e to avoid an excess emissions situation at the end of the monitoring period. As noted below, applications for multi-year monitoring period beginning 2016/17 are also due by October 31, 2017.

To avoid significant costs in this scenario, it is highly beneficial for Facility ‘X’s responsible emitter to submit its initial baseline application and accompanying audit by 30 July 2016.