Publication

National Electricity Market incentives and derivatives under scrutiny

The National Electricity Market (NEM) has been closely examined in two recent government commissioned reviews.

Global | Publication | November 2016

In recent years there have been a series of catalysts, provoking a raft of new domestic and international law geared at countering perceived tax avoidance. Governments and international organisations have moved at unusual speed to introduce new rules governing the way cross-border transactions and arrangements are taxed. We will look at the measures that are on the horizon and consider how these new rules will impact the shipping industry.

Global or international tax law (the body of tax law that governs the way transactions involving one or more countries are taxed) is comprised of international law, such as double tax treaties concluded between two countries and domestic provisions, such as the UK’s own transfer pricing rules.

Historically, countries have had a great degree of autonomy in the way they have taxed international transactions and this has led to mismatches in the way different jurisdictions have treated the same transaction. In some cases, it could even be argued that some countries have adapted their own rules to exploit these differences and encourage transactions to take place through their jurisdiction.

Broadly speaking, international tax laws have the goal of allocating taxing rights, in respect of particular items of income or gains, between two countries that have an interest in a transaction in order to balance the rights of the two countries involved. However, domestic measures often unilaterally protect a country’s ability to raise revenue by levying taxes. “Base erosion and profit shifting”, or “BEPS” is the term which has been given to describe the way in which multinational groups either shift profits from a jurisdiction where they would be subject to a high tax rate to a jurisdiction that taxes them at a lower rate (or not at all), or they reduce the amount of profit subject to tax in their jurisdiction of operation by making “excessive” payments to reduce their tax base. New international and domestic laws preventing BEPS have now been and will be introduced.

The international nature of the shipping industry means that those entities that own, finance and charter ships will need to be aware of the possible implications of these new rules on their businesses.

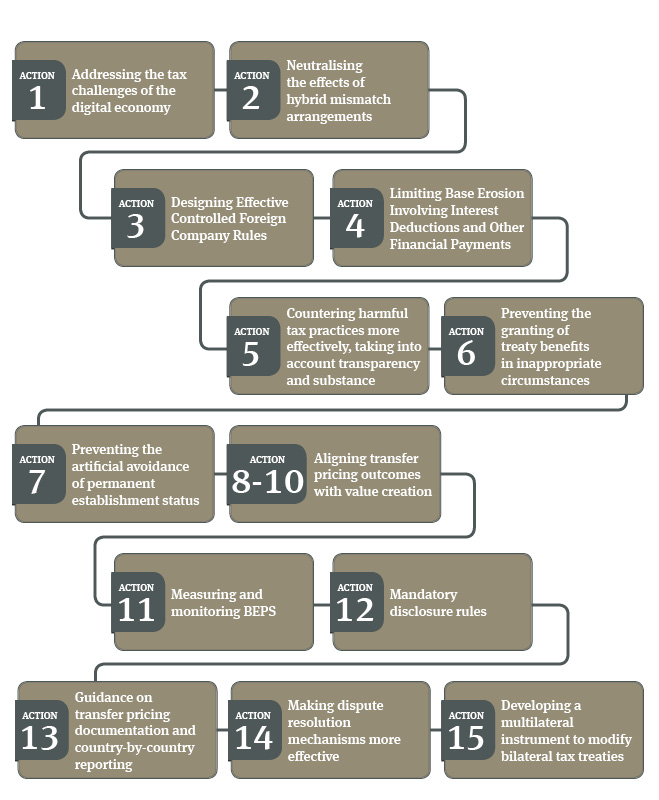

Since 2012, the Organisation for Economic Co-operation and Development (OECD) has been working on 15 action plans which introduce recommendations for how jurisdictions could implement rules to combat BEPS. The final recommendations on these 15 action plans were published in October 2015. Additionally, in the last few months, the OECD has published further guidance and draft guidance which deals with some of these 15 action plans. These are now to be implemented by the relevant countries.

Separately, the EU published in January 2016 a draft directive that recommends minimum standards for EU member states in relation to various tax avoidance techniques. These overlap to some extent with the OECD BEPS proposals, although there are some other recommendations that are specific to the way EU member states should implement their own domestic tax rules on cross-border transactions.

The OECD action plans are:

A number of the action plans above are aimed at the way multinational groups are structured. In particular, the measures under Action 2, Action 3, and Actions 7-10, which in the main relate to transfer pricing between group entities or allocating profits to group entities in lower tax jurisdictions are likely to be important.

Domestic rules dealing with transfer pricing which require an adjustment to reflect arms’ length terms are already in force in most jurisdictions. However, the BEPS proposals go further by aiming to align transfer pricing outcomes with value creation which will include looking at allocating profits in line with the chain of value created within the group. Revised draft guidance was published on 4 July 2016 which discusses how “transactional profit splits” will be applied in order to achieve this aim. Broadly, the “transactional profit split method” looks at the effect that transactions, which are or would be subject to transfer pricing, have on profits by deducing what the profits would have been for the transacting entities if the deal had been on arm’s length terms. As there is value in both the capital invested in vessels and the marketing, vessel management and operation of vessels, the allocation of this value may be contentious, particularly given that different entities will potentially benefit depending on the function they have.

The new measures in relation to the attribution of profits to permanent establishments (PEs) in order to prevent the artificial avoidance of PE status (Action 7) will also potentially impact the shipping industry. Whilst shipping profits are generally protected by double tax treaties, these measures could still be relevant where activities are split between high and low tax jurisdictions, for example, where the owners of vessels are based in a different jurisdiction to the entities which deal with chartering and managing the vessels. Additional draft guidance was also published in relation to these measures on 4 July 2016 which included further discussion of dependent agent PEs (DAPEs) where a non-resident carries on a business in a relevant country via a dependent agent and PEs arising under Article 5(1) of the Model Tax Convention to which the Article 5(4) exemptions do not apply.

Where an owner of a vessel is based in a jurisdiction that imposes withholding tax on outbound payments, Action 6 is likely to become relevant. The specific recommendations under Action 6 are that double taxation treaties should contain either a limitation on benefits article or a “main purpose” article. This will result in further scrutiny of the structures and jurisdictions used in chartering vessels. Those who are party to transactions which relate to shipping may, therefore, want to include provisions ensuring flexibility in the event that measures are introduced to deal with this. Additionally, parties should consider using contractual protections in the event that there is a transfer of the business to a party with less substance than the initial parties to the transaction. These potential new measures are particularly relevant to the shipping industry as it is common for owners to be based in one jurisdiction, with the chartering of the vessel being managed from an office in another jurisdiction.

Additionally, entities involved in the shipping industry will need to look out for the rules that will be introduced under Action 4. This action point will restrict interest deductions where they exceed a certain percentage (likely to be 30%) of earnings before interest, taxes, depreciation, and amortization (EBITDA). The rules are likely to be complex, but it is worth noting that in May 2016 the UK announced that it will proceed with such a restriction in April 2017. These rules are, therefore, beginning to be introduced and are likely to have an impact on those involved in the shipping industry. It will be important to monitor these rules as they are likely to be introduced on a jurisdiction-by-jurisdiction basis and hence involve a degree of inconsistency in their implementation.

Whilst many measures are yet to be implemented, some jurisdictions have already introduced rules to deal with BEPS; therefore, those involved with transactions that could be affected should begin to undertake a risk assessment of the transactions and structures that are most likely to be affected and consider putting effective contingency plans in place.

Publication

The National Electricity Market (NEM) has been closely examined in two recent government commissioned reviews.

Publication

Companies House has announced that from 18 November 2025, companies will no longer be required to maintain registers of directors, directors’ residential addresses, secretaries or people with significant control over the company (PSCs).

Subscribe and stay up to date with the latest legal news, information and events . . .

© Norton Rose Fulbright LLP 2025