Publication

Essential Corporate News – Week ending 11 July 2025

On 1 July 2025, the Quoted Companies Alliance (QCA) published three new board committee guides to accompany the QCA Environmental and Social Guide published in December 2024.

Author:

Global | Publication | November 2016

When amendments to the Canadian take-over bid regime were announced and implemented earlier this year, there was speculation as to the continued relevance and importance of shareholder rights plans (poison pills). After all, the amendments addressed some of the very concerns that shareholder rights plans were originally designed to correct for, namely, by providing directors with more time to consider a bid and seek alternatives and by relieving pressure on shareholders to tender to a bid. Many practitioners, market participants and commentators wondered whether rights plans would continue to be relevant and, if so, what they would look like.

To help answer these questions, we undertook a review of reporting issuers that had publicly disclosed that their rights plans were up for shareholder approval in 2016. In this update, we discuss the results of our review and what it means for the upcoming proxy season.

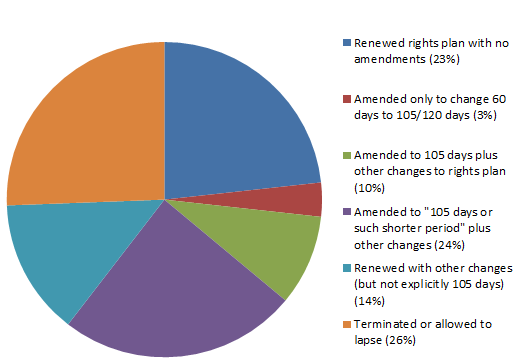

We reviewed the public documents of reporting issuers that disclosed their rights plans were up for shareholder approval in 2016 and that filed information circulars after the amendments were announced. Our findings are as follows:

The actions of issuers during this past proxy season were likely impacted by the timing and effective date of the amendments which, although announced on February 25, 2016, only took effect on May 9, 2016. Of the 23% of issuers that renewed their rights plan without making any amendments, 75% filed their information circulars prior to the effective date of the amendments, suggesting that they were hedging against the possibility of the amendments not taking effect or that the announcement came too late in the proxy season for them to properly consider how best to amend their plan.

Moreover, ISS (Institutional Shareholder Services Inc.) announced at the beginning of March 2016 that, given the new rules would come into force in the middle of the proxy season, it would not update its voting policies for the 2016 proxy season. The one exception was to accept changes to rights plans that extended the minimum bid period for “permitted bids” to 105 days, which ISS stated would be the maximum period supported. This likely also factored into the decision of some issuers not to make any amendments to their rights plan in 2016.

The majority of those issuers that allowed their rights plan to lapse in 2016 cited the belief that the amended take-over bid regime provides sufficient protection against hostile bids. Interestingly, only 14% of the issuers that allowed their plan to lapse have a market capitalization of more than $500 million, while 64% of such issuers have a market capitalization of less than $100 million.

A small majority of issuers that had a rights plan up for renewal during the past proxy season elected to amend their plan. Although several amended only the definition of “permitted bid” to change the minimum period that a bid must remain open from 60 to 105 days, the majority made more comprehensive amendments.

Both ISS and Glass Lewis just released their proxy voting recommendations for the 2017 proxy season, and in both cases they formally amended their policies to increase the permitted bid periods to align with the new minimum deposit period required by the amended bid regime. Their updated policies state they will consider management proposals to ratify a rights plan on a case-by-case basis and will recommend voting against a rights plan with a permitted bid minimum period of greater than 105 days (instead of 60 / 90 days pursuant to their old policies). Otherwise, neither ISS nor Glass Lewis made any changes to its recommendations regarding rights plans.

So…what should issuers with a rights plan up for renewal in 2017 do? Renew the rights plan (with appropriate amendments) or allow it to lapse? And should issuers without a rights plan consider implementing one? The answer depends on the particular circumstances of the issuer.

While the new take-over bid rules address some of the perceived timing and fairness issues that rights plans were intended to address, they do not protect issuers against creeping (exempt) take-over bids for control (such as the accumulation of 20% or more of the issuer’s shares through stock exchange acquisitions, or the acquisition of a control block through private agreement purchases from a few large shareholders). Shareholder rights plans preclude creeping take-over bids, ensuring that all shareholders have an equal opportunity to share in the payment of a control premium.

The protection against creeping bids is the most compelling reason for issuers to have a rights plan. In assessing the need for a rights plan, an issuer should carefully consider the likelihood of a creeping take-over bid by scrutinizing its shareholder base (for example, to identify shareholders at or above the 10% level, which are required to file early warning reports under Canadian securities laws).

If a rights plan is to be renewed or implemented, the following are amendments that should be considered in order to be in line with the new take-over bid rules, institutional guidelines and market practice:

While more extensive structural amendments could be considered to reduce duplication with the new take-over bid rules, the above more straightforward amendments are in line with market practice and institutional guidelines.

Should you wish to have more information on making specific amendments to suit your issuer’s rights plan, please do not hesitate to contact us.

The amendments to the take-over bid regime can be accessed here.

The ISS and Glass Lewis proxy voting recommendations for the 2017 proxy season can be accessed here and here.

Our earlier commentary on the legislative amendments can be accessed here and here.

Publication

On 1 July 2025, the Quoted Companies Alliance (QCA) published three new board committee guides to accompany the QCA Environmental and Social Guide published in December 2024.

Publication

In the two years since our last climate litigation update, the prevalence and variety of global climate litigation around the world has continued to increase.

Publication

Selon un rapport conjoint du Bureau du surintendant des institutions financières (BSIF) et de l’Agence de la consommation en matière financière du Canada (ACFC), environ 70 % des institutions financières fédérales prévoient utiliser l’IA d’ici 2026 .

Subscribe and stay up to date with the latest legal news, information and events . . .

© Norton Rose Fulbright LLP 2025