Publication

General Counsel & Legal Operations Forum

We will be participating in Consero's General Counsel & Legal Operations Forum from 17–19 September 2025 at Sopwell House in St Albans, UK.

Global | Publication | July 2017

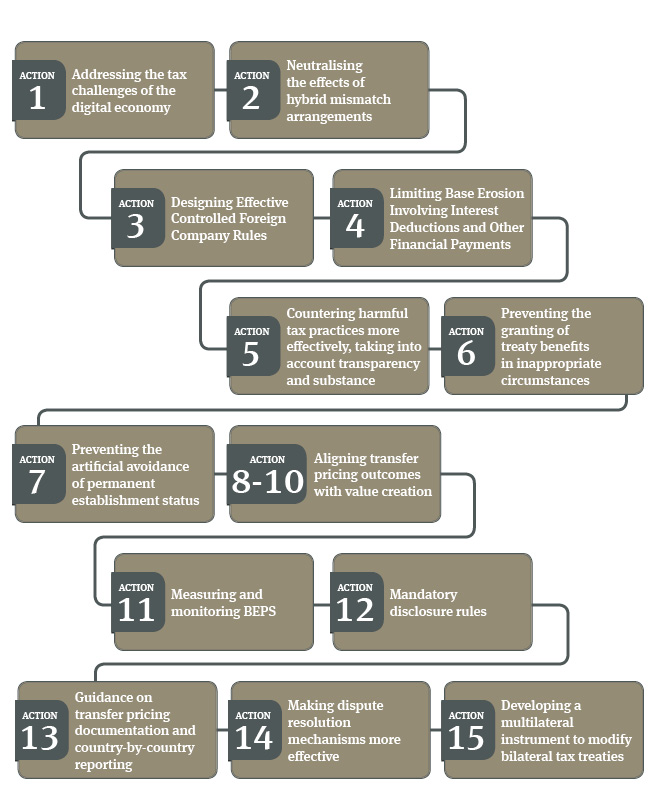

In June 2017, sixty-seven states signed the OECD’s Multilateral Convention to Implement Tax Treaty Related Measures to prevent BEPS (the “Multilateral Instrument” or MLI). The MLI was introduced as part of the OECD’s base erosion and profit shifting project (BEPS), which we wrote about in June 2016, International aviation and international tax avoidance. BEPS has 15 actions shown in Figure 1 and the MLI implements some of the actions directed at preventing tax avoidance by the use of cross-border structures. Its purpose is to allow changes to be made to bilateral tax treaties on a multilateral basis, so that it is not necessary to renegotiate every single bilateral tax treaty between the participating states.

Many aircraft finance transactions rely on double taxation treaties to ensure there is no withholding tax on the payment flows (whether on a lease or on a loan). Parties to those transactions should consider whether the implementation of the MLI could have an impact on the ability to rely on a particular tax treaty.

Figure 1: BEPS - 15 actions

The MLI contains a series of provisions that are regarded as good practice or minimum standards by the OECD in order to prevent cross-border tax avoidance. It also contains various optional provisions that have a similar effect. States that sign up to the MLI are entitled to choose which of their double tax treaties will be amended by the MLI, and which of the optional measures of the MLI will apply to those treaties. If two states to a bilateral treaty agree that a measure will apply to it, then the bilateral treaty is treated as having been supplemented by the revised provision. This means that bilateral treaties covered by the MLI will contain measures to prevent treaty abuse.

Where an aircraft lessee is based in a jurisdiction that has a withholding tax on aircraft lease rents, the action point on “treaty abuse” is likely to become relevant. The MLI will amend relevant treaties so that they contain minimum standards to prevent treaty abuse. This will be done by introducing either a limitation on benefits article or a “main purpose” article. States are free to adopt a standard which exceeds the minimum standard. The OECD have published the expected position that each of the sixty-seven states are likely to adopt.

The MLI will enter into force three months after the date when the number of states ratifying it reaches five. One exception is that a state can choose to delay its implementation until the start of the next taxable period. When the MLI enters into force it will apply to withholding taxes only. Six months after the MLI has entered into force it will take effect for other taxes.

The current expectation is that five states will have ratified the MLI by 30 September 2017. If this happens, then it is expected to generally apply to withholding taxes from 1 January 2018 for those states that have ratified it and to other taxes from 1 July 2018.

The changes introduced by the MLI could result in more scrutiny of transactions involving intermediate lessors that rely on treaty protection to receive rentals without withholding tax. Some states are already beginning to look at such arrangements, questioning whether the intermediate lessor has appropriate “beneficial ownership” of the lease rentals for tax treaty purposes Some jurisdictions are introducing their own rules, separate from the MLI, to deal with what they perceive to be the inappropriate use of a tax treaty. This will allow them to impose measures combatting treaty abuse, regardless of whether their treaty partners first agree.

Generally, the risk of withholding taxes under an aircraft lease is allocated to the lessee where the withholding tax arises as a result of a change of law. The rationale for this is that withholding taxes are generally imposed by the jurisdiction of the paying party, which would generally be the lessee jurisdiction. However, any restriction on treaty benefits arising as a result of the implementation of new anti-abuse provisions under the MLI might equally be triggered because of a lack of substance or commercial rationale for the lessor entity (and accordingly one might think the “fault” should lie with the lessor rather than the lessee in these circumstances). Therefore, parties will need to consider whether to introduce specific provisions into new aircraft leases to deal with the possibility of changes to double taxation treaties as a result of the implementation of the MLI; similarly, lessees may want to review existing leases to establish which transactions might be more vulnerable to the imposition of the MLI.

It should be noted that the US has not signed up to the MLI and is not expected to do so. As a result, no treaties where the US is a contracting party will be amended by the MLI.

Publication

We will be participating in Consero's General Counsel & Legal Operations Forum from 17–19 September 2025 at Sopwell House in St Albans, UK.

Publication

Pacific Island nations face existential threats from climate change, particularly from rising sea levels that risk submerging ancestral lands and displacing entire communities.

Publication

The insurance industry is facing a rapidly changing litigation environment. Emerging risks, regulatory developments, and technological advancements are reshaping how insurers approach underwriting, claims, and risk management. Below is an overview of the most significant trends impacting the sector.

Subscribe and stay up to date with the latest legal news, information and events . . .

© Norton Rose Fulbright LLP 2025