1. Is it an acquisition within the scope of the regime?

Acquisitions of the following are within scope:

- Acquisitions of:

- Shares, units or interests in managed investment schemes where control is gained or a significant change in interest occurs*, or

- Acquisitions of assets.

- That are ‘connected with Australia’, meaning the target entity carries on business in Australia or the asset is located in Australia.

*From 1 April 2026, certain acquisitions must still be notified to the ACCC even though ‘control’ may not be acquired, where an acquisition results in voting power traversing across thresholds of 20 per cent and 50 per cent.

2. Acquisitions that do not fall within the scope of the regime

Acquisitions of the following are outside the scope:

- Acquisitions of 20 per cent or less voting power in an Australian listed company, listed scheme or a large unlisted company;

- Internal restructures and re-organisations;

- Acquisitions of assets in the ordinary course of business (OCB);

- Certain land and quasi-land acquisitions, including acquisitions:

- In the OCB, which may include office leases

- For any purpose by a business primarily engaged in buying, selling, leasing or developing land, other than to operate a commercial business on the land that is not ancillary or incidental to the primary purpose

- In relation to residential property development

- Lease extensions or renewals

- Sale and leaseback arrangements

- That are multi-staged, where the previous stage resulted in an acquisition of an equitable interest in the same land before 1 January 2026, or was notified/waived;

- Acquisitions during external administration or transfer of members’ benefits between superannuation entities.

- Certain financial market acquisitions, such as clearing and settlement facilities, or debt instruments and derivatives that do not result in control.

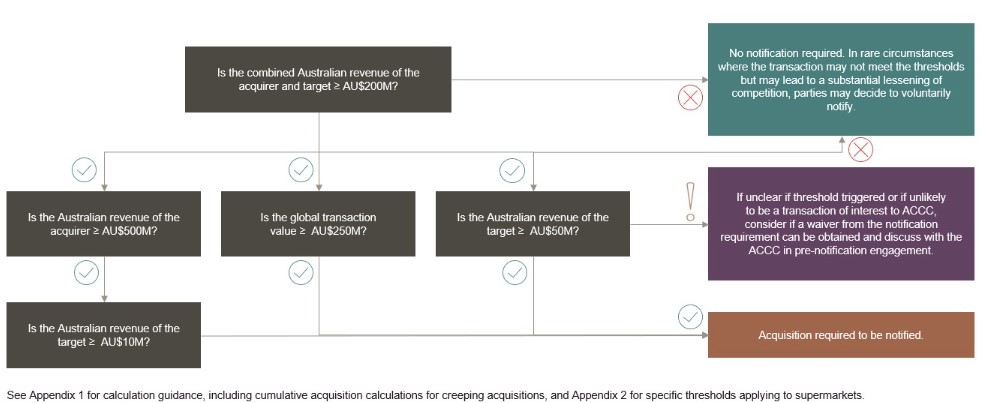

3. Does the deal trigger the notification thresholds?

Most deals will be subject to the following notification thresholds:

Different thresholds have been introduced for acquisitions that do not comprise all, or substantially all, of the assets of a business (discrete asset acquisitions).

From 1 January 2026 until 31 March 2026, a discrete asset acquisition requires notification if the combined Australian revenue of the acquirer group and target >AU$200m AND the global transaction value is >AU$250m. (For conservatism, we are still keeping an eye on the revenue attributable to the target asset (if any) to assess filing obligations due to some inconsistency between the statutory instrument and the explanatory materials.)

As of 1 April 2026, a discrete asset acquisition requires notification based on decreased global transaction value thresholds:

- Combined Australian revenue of the acquirer and target >AU$200m, AND global transaction value is >AU$200m; OR

- Acquirer’s Australian revenue >$500m, AND global transaction value >$50m.

See Appendix 1 for threshold calculation guidance, and Appendix 2 for specific thresholds applying to supermarkets.

4. Is a waiver available?

Notifiable acquisitions must not proceed without ACCC clearance or a waiver.

The waiver process is an alternative to notification, not an initial step. Its suitability depends on a careful assessment of the acquisition's complexity and competitive impact.

Waiver applications are best suited for acquisitions that can be quickly assessed based on initial information and:

- Clearly do not raise competition issues (e.g., no competitive overlaps, low market shares, no vertical integration, or bundling concerns), and/or

- Are unlikely to exceed monetary thresholds or may do so under a technicality.

In contrast, a full form notification is required for acquisitions that clearly meet thresholds and may raise competition issues.

While waivers provide a more cost-effective and streamlined pathway, they still require information on market structure, estimated revenues, commercial rationale and more. If initial waiver application information is insufficient or raises any concerns, the ACCC will reject it. This necessitates beginning again with a full notification and additional filing fee.

5. What does the notification process look like?

Step 1: Pre-notification engagement with the ACCC. Parties are to provide a draft notification application and all transaction documents to allow the ACCC to identify if further information is needed.

Step 2: Parties complete and submit a long or short notification form via the ACCC’s online acquisitions portal.

The long form is required where:

- For acquisitions of a competitor: Estimated market share post-acquisition is:

- ≥ 40 per cent and the increment resulting from the acquisition is ≥ 2 per cent OR

- ≥ 20 per cent – 39 per cent and the increment resulting from the acquisition is ≥ 5 per cent.

- For acquisitions within supply chains, the party:

- In the upstream market has a market share ≥ 30 per cent and the other party has a downstream market share of ≥ 5 per cent.

- In the downstream market has a market share ≥ 30 per cent and the other party has an upstream market share ≥ 5 per cent.

- For acquisitions by conglomerate: The parties supply adjacent products or services and one of the parties to the acquisition has a market share ≥ 30 per cent.

- For acquisitions that are otherwise sensitive: Including where the target is a vigorous and effective competitor, is developing a significant product, or where the acquisition is of a business that supplies or controls a key input.

Step 3: The ACCC will confirm the effective notification date (after the filing fee is paid) and the review timeline will begin.

The filing fee to be paid to the ACCC with the notification is predetermined for each stage or pathway.

| Stage |

Transaction value (if applicable) |

Fee |

| Notification waiver |

n/a |

AU$8,300 |

| Phase 1 |

n/a |

AU$56,800 |

| Phase 2 - depending on transaction value |

AU $50 million or less |

AU$475,000 |

|

More than AU $50 million but not more than AU $1 billion |

AU$855,000 |

|

More than AU$1 billion |

AU$1,595,000 |

| Public benefits application |

n/a |

AU$401,000 |

|

|

|

Acquirers that are small businesses, i.e. have less than AU$10 million revenue in the previous financial year, are exempted from paying the fee.

6. How long will the ACCC review take?

| Phase |

Timing |

Waiver

|

The maximum timeframe for the ACCC to complete its assessment is 25 business days. If no determination is made in this time frame, the waiver application will be deemed to be denied.

|

|

Pre-notification discussions

|

The ACCC will engage ‘promptly and meaningfully’ with businesses once a request is received. The ACCC recommends that parties initiate pre-notification engagement at least two weeks before formal notification and earlier for acquisitions which may raise competition concerns.

|

|

Phase 1

(15-30 business days)

|

There will be an initial ‘Phase 1’ review process of 30 business days, from a complete application being lodged. Most deals are expected to clear in this timeframe. There will also be scope for a fast-track determination by the ACCC after 15 business days if no competition issues arise.

|

|

Phase 2

(+90 business days)

|

A ‘Phase 2’ review will be more in-depth and will take up to a further 90 business days. At the end of Phase 2, the merger can be put into effect with or without conditions or disallowed by the ACCC entirely. The ACCC cannot block a merger unless a Phase 2 review has occurred.

|

|

Public benefit assessment (+50 further business days)

|

From 2026, approval on the basis that there are substantial public benefits that outweigh anti-competitive downsides, is only able to be sought by merger parties if the ACCC blocks the deal in Phase 2. The prescribed period for this review is an additional 50 business days.

|

|

Regime promotes timing discipline but the clock can be stopped

|

If an ACCC determination is not made within the statutory timeframe for Phase 1 or Phase 2, the acquisition will be deemed approved. This is a significant shift from the current flexible timeframes for reviews in the informal regime that can be varied unilaterally by the ACCC. However, in practice we would expect the ACCC to utilise ‘stop the clock’ mechanisms to extend the statutory timelines thereby providing some flexibility.

|

| Post-clearance waiting period |

Deals cannot close for 14 calendar days after ACCC clearance occurs to allow any applications for review to be made. |

| |

|

7. Other important aspects

- Implications of not notifying: Putting a notifiable transaction into effect (including certain pre-completion coordination with the target/purchaser) without receiving clearance of a notifiable transaction is a breach of the Act and significant penalties may apply. It will also render the transaction void. Changes have been flagged to remove automatic voiding during 2026.

- The substantive test: The ACCC must be 'satisfied' that a notified acquisition would have the effect or likely effect of substantially lessening competition in order to oppose it proceeding.

- To address “creeping acquisitions” the new law:

- Makes clear that a substantial lessening of competition arising from a merger can include creating, strengthening or entrenching a substantial degree of market power.

- Enables the ACCC to look at all transactions undertaken by a party to the notified acquisition that are valued at more than $2 million and connected to Australia in the past three years in assessing the impact of the notified acquisition and in applying the thresholds.

- Uncaptured transactions: The ACCC will monitor acquisitions and will take appropriate investigatory and enforcement actions in respect of anti-competitive acquisitions, even if they fall below the thresholds for mandatory notification.

- Review will be public: The ACCC will publish the key details of the transaction within one business day of a notification. Waiver applications will also be published for third-party consultation, subject to limited exceptions.

- Restraints in sale documents: The ACCC will have the power to review and invalidate restraints if it considers they go further than necessary to protect goodwill.

Appendix 1: Monetary thresholds calculation methodology

The approach to calculating revenue and transaction values is similar to that which applies in many jurisdictions.

1. Calculate the Australian revenue of all parties to the transaction

| Each principal entity acquiring control |

The target |

|

Australian revenue of the previous financial year of each principal party to the acquisition and each of its ‘connected entities’ (‘acquirer group’).

In effect, this looks at the Australian Revenue of the entire corporate group involved in the transaction.

|

- Acquisition of shares: Australian revenue of the previous financial year of the target and each of its connected entities (‘target group’).

- Acquisition of all, or substantially all, of the assets of a business: Australian revenue of the target group to the extent that it is attributable to the asset.

|

| |

|

Cumulative acquisitions: In calculating if the target revenue thresholds are met, Australian revenue or assets of the target group need to be considered in combination with that of past acquisitions within the previous three years of target businesses that are predominately active in the same or similar market.

For past acquisitions by the acquirer group Australian revenue is calculated at the time of the respective signing date.

However, the following acquisitions by the acquirer group of previous targets can be disregarded:

- With Australian revenue below AU$2m;

- That are not ‘connected to Australia’;

- That was already notified to the ACCC;

- Of not all or substantially all of a business;

- Of assets that have subsequently been divested or disposed;

- That have not closed at the time of the test, i.e. acquirer does not yet control target.

2. Consider the transaction value

In measuring a transaction’s value, the greater of the following applies:

- The market values of all shares and assets being acquired; or

- The consideration received or receivable for all of the shares and assets being acquired.

3. Notes on revenue and values

- Filing forms: the forms require reporting of historical Australian revenue for three years.

- ‘Australian revenue’ means the amount of gross revenue, determined in accordance with accounting standards, of the most recently ended financial year that is attributable to transactions or assets within Australia, or transactions into Australia.

- ‘Connected entity’ is broadly defined and uses concepts of both:

- legal control (i.e. where an entity controls the Board composition, 50 per cent of the voting rights or 50 per cent of the share capital of another entity), and

- practical control, i.e. where an entity has the capacity to determine decisions about another entity’s financial and operating policies either alone, with associates or as a Special Purpose Vehicle (SPV). An entity with standard minority shareholder protection rights that do not confer control will not be considered to be an associate.

- Target group revenue considerations do not include revenue of any other entity not acquired as a result of the acquisition (for example seller revenue is not included in target group revenue).

Appendix 2: Notification mandatory for groceries

While the preceding notification thresholds apply generally across the economy, certain transactions within the supermarket sector must be notified regardless of whether they meet the general notification thresholds and regardless of whether they result in a change in control.

Major supermarkets – Coles and Woolworths (including their connected entities) – must notify the ACCC of acquisitions of shares or assets where they are acquiring:

- A supermarket business (in whole or in party, i.e. a business engaged in the retail supply of grocery products).

- Land for supermarket business, i.e. a legal or equitable interest in land (in whole or in part) that meets certain land size requirements (> 1,000m2 for a commercial building or > 2,000m2 for land).

Specific land acquisitions for supermarket business are exempted from the notification obligation:

- A lease extension or renewal for land that has currently operating commercial business.

- A subsequent acquisition in the same land that was subject to a previously notified acquisition.

- Acquisitions of land interest in the form of land development rights.

- Acquisitions related to a sale or leaseback arrangement relating to the land.

- Acquisitions of land upon which another non-supermarket business is operating or will operate.